New Gallup survey data suggest that about 12 million previously uninsured Americans have gained coverage since the fall.

By Noam Levey

5:56 PM PDT, April 16, 2014

WASHINGTON — President Obama's health law has led to an even greater increase in health coverage than previously estimated, according to new Gallup survey data, which suggests that about 12 million previously uninsured Americans have gained coverage since last fall.

That is millions more than Gallup found in March and suggests that as many as 4 million people have signed up for some kind of insurance in the last several weeks as the first enrollment period for the Affordable Care Act drew to a close.

Just 12.9% of adults nationally lacked coverage in the first half of April, initial data from the Gallup-Healthways Well-Being Index indicate. That's the lowest rate since the survey began in 2008.

Eighteen percent were uninsured in the third quarter of 2013, just before Americans could start shopping for coverage on the new online marketplaces created by the law.

Gallup pollsters cautioned that the data are preliminary but said it is increasingly clear the health law is responsible for the gains. "It is fair to say it is having a significant impact," said Dan Witters, the survey's research director.

Critics of the law, sometimes called Obamacare, say it has done little to expand health coverage.

Gallup's latest data, which parallel recent findings from Rand Corp. and the Urban Institute, lump together all coverage gains, including those on the marketplaces, as well as through other forms of insurance, such as Medicaid, employer-provided coverage and health plans purchased directly from insurers.

The data also take into account any losses in coverage the law may have brought about by the cancellation of health plans that did not meet new standards.

The health law enables Americans who do not get coverage through an employer to select a plan on government-run marketplaces. Insurers must offer a basic set of benefits and can no longer turn away sick customers.

Americans making less than four times the federal poverty level — about $94,000 for a family of four — qualify for government subsidies in most parts of the country.

In about half the states, very low-income Americans can sign up for Medicaid. Most Republican-led states, however, have not expanded the program to cover all low-income residents, an option provided by the health law.

The disparity between states that have embraced the health law and those fighting it is already showing up in health coverage, Gallup found.

From 2013 to the first quarter of 2014, the uninsured rate fell to 13.6% from 16.1% in the 21 states that are expanding Medicaid and are fully or partially operating their own marketplaces, rather than deferring that job to the federal government.

The uninsured rate dropped about a third as much in the states that have not fully embraced the law, to 17.9% from 18.7%, the poll found

"The gap is widening," Witters said.

The Obama administration reported last week that 7.5 million people have signed up for coverage through the marketplaces.

Not all of these people were previously uninsured, however. Some probably had coverage through an employer. Some may have bought insurance directly from an insurance company. Others may have been on government programs, such as Medicaid.

Gallup's polling does not clarify how many of the 7.5 million were previously uninsured, nor does the survey identify whether the newly insured got coverage on a marketplace or through other avenues, such as Medicaid or an employer.

The new data do provide some new insights into who the newly insured are, however.

They appear to be slightly younger than the population at large, with two-thirds ages 18 to 49, compared with 55% of the population at large.

And they are about as healthy as the general population, according to self-reported health status.

The newly insured also seem to reflect the nation's deep political divide over the health law; 54% are Democrats, while just 24% are Republicans.

Frank Newport, Gallup editor in chief, said that suggests Americans' political leanings may be influencing their decisions about whether to get health insurance. Gallup has found that although about 3 in 4 Democrats approve of the health law, just 1 in 6 Republicans do.

Gallup interviews about 14,800 adults a month nationwide for the Gallup-Healthways Well-Being Index, making it one of the largest health insurance surveys in the nation.

The Conservative Case Against Obamacare: A Restatement

Since Obamacare “hit” its “enrollment” “target,” Democrats, liberals, and their friends in the press have enjoyed some old-fashioned taunting of Republicans. This would be justifiable if a.) Republicans had destroyed the website that needed fixing or b.) predicted that nobody would sign up for the program in the first place.

Neither condition holds, of course. The website was totally the design of CMS, HHS, and the White House, which are all run by Democrats. Meanwhile, as Michael Cannon argued, it is no big feat to get people to sign up for a heavily subsidized product.

All of this Democratic triumphalism makes it a good time to restate in summary form the conservative case against Obamacare.

For starters, its recent success is grossly overstated.

Eight million “enrollments” is an enormous exaggeration, so much so that you cannot in good faith say that Obamacare “beat” its expectations. In fact, last week the Congressional Budget Office stuck with its most recent prediction of 6 million enrollments:

CBO and JCT estimate that, over the course of calendar year 2014, an average of 6 million people will be covered by insurance obtained through the exchanges. The total number who will have such coverage at some points during the year is expected to be more than the average because some people will be covered for only part of the year.

The 6 million number is not, and apparently never was, the number of paid subscribers arrived at when the enrollment period ended. And why should it be? That has become a politically important number, but from a federal budgetary perspective, a coverage perspective, or an insurer financial perspective, it has no value. What really matters is the annual average.

So, is CBO’s 6 million still justifiable as an estimate? If we take the administration at face value on its monthly enrollment numbers, assume that 90 percent of initial enrollees pay their first month premium, and then a 1 percent non-payment rate thereafter, the annual average for 2014 would be about 5.5 million, and the final enrollment as of December would be about 6.6 million.

It is worth noting on this front that a study from the U.C. Berkeley Labor Center projects that 40 percent of enrollees in Covered California will leave the individual market by the end of the year, either migrating to employment based insurance or Medicaid.

Whether this estimate turns out to be true, or whether California is indicative of the rest of the nation, is beside the point, which is this: The paid enrollment prediction made by CBO and adopted last year by the White House is substantially different than the numbers promulgated by the White House. In reality, the White House has invented a statistic that has no policy relevance whatsoever, and successfully sold it to a credulous press corps frustrated by the website’s collapse and eager for good news. Additionally, as insurance industry expert Robert Laszewski has noted, it would not be all that hard for the White House to compile and release the data relevant to the actual performance of the program. That the White House has not done this, nor has any plans to do so, should tell you everything you need to know.

The most fair assessment of Obamacare, given the data constraints imposed by the president for political purposes, is that the program will probably get in the neighborhood of 6 million paid enrollments on average this year, which is what CBO predicted earlier this year, but is just 67 percent of what the budget scorekeepers predicted would happen after the Supreme Court ruling.

Conservative objection #1: Obamacare has no legitimate funding mechanism.

page 2

Sure, the Congressional Budget Office says it is “paid for,” but one must be careful to read the fine print of every CBO report. It is the very model of a good faith agency in the government, but CBO must still render its judgment based on scoring conventions that can be gamed by legislators.

Chuck Blauhaus of the Mercatus Center recently released a thorough review of the program's financing problems. Here is just a brief summary of what’s wrong:

a.) It cut the Medicare Part A Hospital Insurance (HI) Fund in ways that CMS thinks will be politically unsustainable. These cuts are back-ended into the later years of the CBO scoring range, a typical trick for legislators who want to use unfeasible means to pretend to keep deficits in line.

b.) It double counts money taken from the HI Fund. Because of peculiar CBO scoring conventions, money taken from Medicare Part A is not scored as borrowed money, even though it in fact is intragovernmental debt.

c.) It cuts Medicare Advantage in ways that even congressional Democrats, including those who voted for the law in the first place, pressured the White House to restore.

page 3

There is no doubt that some will be made better off because of Obamacare. It closes the Medicare Part D “donut hole.” Many people will get a good deal thanks to the subsidies, despite increased costs and narrow networks. It provides coverage to people with pre-existing conditions. It allows young adults under 26 more time on their parents' insurance plans. This is why no serious conservative opponent ever declared that nobody would join Obamacare. It is why serious conservatives have put together policy alternatives that help these people.

However, the law makes losers out of a vast array of people, whose economic status usually makes them “off the table” when it comes time to fund new social welfare programs.

Consider:

a.) Seniors on fixed incomes will see their Medicare Advantage costs go up.

b.) Seniors' access to hospitals will be diminished because of cuts to the Hospital Insurance Fund.

c.) Many in the small group marketplace will see their costs go up and coverage options decrease, but will not be eligible for subsidies.

d.) Many kicked off their existing plans, especially those with sensitive medical conditions, had to experience grave uncertainty as to whether their new coverage would be sufficient. When the special exemption for old plans ends in a few years, many more will experience the same uncertainty.

e.) Many in the individual marketplace will see their costs go up and coverage options decrease, despite the subsidies (assuming they are eligible for them).

f.) Many will not find sufficient value in any of the plans, and choose instead to pay the mandate penalty and remain uninsured.

g.) Rural communities where competition is sparse and enrollment weak will see premiums increase more relative to urban areas where those conditions don’t hold.

h.) The premium support formula results in young people at a given income level subsidizing older people at the same level, despite the fact that the latter are finishing up their peak earning years and should be more able to pay.

For a comprehensive accounting of the program’s winners and losers, see this interesting analysis by Chris Conover of Duke University.

Importantly, none of these people had to be harmed. In fact, this is of a piece with the previous critique: it all has to do with hiding the true costs of the program. To do that, congressional Democrats and the president not only used a series of phony cuts and tax increases, they alsospread the burdens of the bill far and wide, so that these people are paying an implicit tax to expand coverage.

Look again at these aforementioned “losers,” and you will see that they are not, by and large, the richest 1 percent, 5 percent, 10 percent, or even 20 percent. For instance, premium subsidies disappear for an individual making $45,000 per year, or a family of four making $90,000; and prior to these thresholds, the subsidies become quite measly relative to the cost of insurance. These are middle class people whose condition in this economy is often tenuous. Medicare serves the entire elderly population, which means these cuts are going to cut across income lines. The people who find insufficient value in exchange plans, and choose instead to pay the fine, will almost assuredly be middle income people, often young. A 25-year old making $50,000 is probably not in as good a shape economically as the 60-year old in the same condition whom he subsidizes, as the former still has student loan debt and is soon to take on mortgage debt.

These people should not have been harmed for any reason, let alone reasons of political convenience.

Conservative objection #3: Obamacare restricts choices and increases costs.

Liberals have been trumpeting CBO reports that talk about insurance premiums coming down. This is misleading for two reasons. First, they are coming down relative to CBO projections made at the time the bill was passed. In real terms, premiums have been going up. Check out this analysis from the Manhattan Institute. Also, consider these estimates from the American Enterprise Institute on how young people in particular will pay more. Also, see this study from Morgan Stanley showing a dramatic spike in premiums over the last six months. And premiums, of course, are only one way to increase the burdens on consumers. Co-pays and deductibles have also gone up.

Meanwhile, lost in the media's celebration of CBO’s announcement of low premiums was the fact that premiums came in lower than expected in part because insurers cut provider networks, a reality that new enrollees are already experiencing. In California, they’ve taken to calling it “medical homelessness.”

All of this is a consequence of two policy decisions made by the Democrats. First, they chose to allow relatively sick people to pay the same price for health insurance as relatively healthy people. Those extra costs must be borne somewhere, and they are coming in the forms of higher premiums, copays, and deductibles, and narrow networks. Second, they mandated that insurers cover a vast array of health services, regardless of whether people want them. Again, that costs money, and for many people these benefits provide little or no value.

The only way the country becomes more prosperous is through the creation of jobs in the private sector. The government cannot create wealth. It can only redistribute it, and Obamacare burdens businesses through its vast redistributive program. There are the administrative burdens, the employer mandate, and the requirements that insurance must take a certain form.

Conservative objection #5: Obamacare is probably unsustainable ... in the long run.

Conservatives who understand how the law works were not predicting a death spiral as of last fall, when the exchanges were supposed to work. For a time, it looked like it might happen because of technical problems, but that was not the original prediction.

Instead, the expectation is that the weak mandate to purchase insurance, plus the fact that Obamacare is a bad deal for many people, would make it disproportionately attractive to older and sicker individuals, the types for whom the program is a good deal but who cannot make an insurance market prosper.

Why will this only happen in the long run? The answer has to do in part with three Obamacare programs designed to serve as a backstop for insurers: risk corridors, reinsurance, and risk adjustment. Reinsurance pays marketplace insurers for their losses per patient from a tax on everybody else's insurance. Risk corridors are supposed to transfer funds between insurers based on profit and loss margins, but leaves open the potential for government funds going directly to insurers. These two programs end after 2016, which means by that point Obamacare will have to stand on its own, without the feds guaranteeing insurer profits.

Conservatives think the weak mandate, combined with the higher costs and relatively small value for many people, means that after these backstops go away the program will struggle. Whether that results in a “death spiral,” or simply increasing costs for the federal government through ever-larger premium tax credits, is another matter. Historically speaking, the better bet is unsustainability because of evermore costs to the taxpayer. That is the core problem with Medicare: the program was designed in a way that grew costs far beyond the capacity of the funding mechanism to keep up. For this reason Medicare is set to hit a crisis point in the next decade. Conservatives think that Obamacare will suffer a similar fate, perhaps sooner.

In conclusion, any one of these objections would merit virtually uniform opposition from conservatives to Obamacare. But take them all together, and most American conservatives have arrived at the same conclusion: this law is fatally flawed, must be repealed entirely, and replaced with something that is sustainable and not overly burdensome to taxpayers, middle class families, or businesses. After all, fixing each of these problems would result in a new law that bears only the faintest resemblance to Obamacare as it is today.

Moreover, a lot of conservatives believe that liberals have the exact same opinion. While publicly applauding the expansion of coverage, some of them must understand the grave problems inherent to this law. This helps explain the sense on the right that, for liberals, this is simply a stalking horse for single payer: first, sign up new people under a federal entitlement that cannot practically be taken away, then deal with the various harms to middle class voters, burdens on businesses, and extreme cost overruns … by proposing “Medicare for all.”

The irony here is rich indeed: the very same liberals who prefer such a “repealing and replacing” of Obamacare are actually criticizing Republicans for wanting to repeal and replace with a conservative alternative.

This newest monthly Kaiser Health Tracking poll, which has provided some of the most reliable data on the public's opinion interaction with the Affordable Care Act over the past four years, finds that nearly 4 in 10 uninsured adults cited affordability as their main reason for skipping health insurance coverage. Twenty-two percent cited employment reasons (they were unemployed or couldn't get coverage through their job), while another 11 percent said they missed the deadline and 9 percent said they just didn't want insurance.

Most Americans don't think Obamacare hit its enrollment target, a new Kaiser Family Foundation poll finds. Nearly six in 10 Americans (57 percent) said the law fell "short of expectations" on sign-ups.

Vermont’s case for single-payer health care can be summarized in one number: $82,975. That’s the amount a 2011 study in the journal Health Affairs found the average American doctor spends on dealing with insurance companies. Across the border in Ontario, doctors spend about a quarter of that amount — $22,205 per physician — interacting with the province’s single-payer agency.

In September 2013, CNBC found that 46 percent of the public said they were opposed to "Obamacare," but only 36 percent of the public said they were opposed to "the Affordable Care Act." In other words, the name Obamacare boosted opposition by 10 percentage points. The disconnect runs deeper. The Kaiser Family Foundation has found that the component parts of Obamacare poll highly even as the law itself remains unpopular. They also found that Obamacare's most popular provisions were its least well-known, and vice versa:

Dean Angstadt hated the Affordable Care Act with intense partisan fervor until it saved his life. "[T]his year … a faulty aortic valve almost felled Angstadt," writes Philadelphia Inquirer reporter Robert Calandra. "Suddenly, he was facing a choice: Buy a health plan, through a law he despised, that would pay the lion's share of the cost of the life-saving surgery—or die. He chose the former." Now he's proselytizing for Obamacare.

In 2006, Massachusetts began requiring health insurance coverage for nearly all residents – years before the rest of the country. Now a study shows that after the reforms went into effect, the state saw a 2.9 per cent decrease in the death rate through 2010. According to the study, which was led by Benjamin Sommers of the Harvard School of Public Health in Boston, that translates to around 320 lives saved every year. The finding hints at the benefits that may soon be felt in the rest of the US, where since October millions of Americans have signed up for insurance under the federal Affordable Care Act (ACA), which is modelled on the Massachusetts system.

Sen. Mitch McConnell has a very strange new position on Obamacare. The Republican Senate minority leader is rhetorically standing by his pro-repeal stance, but -- in what amounts to a softening of his position and a contradiction -- he's also saying his home state of Kentucky should be allowed to keep Kynect, its state-based Obamacare exchange, if the federal law is eliminated.

It's a relief to see so much outrage over poor access to government-provided health-care benefits. But it would be nice to see bipartisan outrage extend to another unfolding health-care scandal in this country: the 4.8 million people living under the poverty line who are eligible for Medicaid but won't get it because their state has refused Obamacare's Medicaid expansion. As appalling as the wait times are for VA care, the people living in states that refused the Medicaid expansion aren't just waiting too long for care. They're not getting it at all. They're going completely uninsured when federal law grants them comprehensive coverage.

Since the Affordable Care Act's passage, the laws opponents have outspent its supporters 15:1. And though the law beat enrollment expectations its launch was an extraordinarily high-profile disaster — so much so that the public still thinks Obamacare has fallen short of its sign-up goals.

In the end, was this really worth closing the government for or even threatening to default on US debt?

Major New Study Says Obamacare Is Working — Even For Republicans

The Affordable Care Act has been successful at achieving some major goals in the first year of its full implementation, according to a new study from The Commonwealth Fund.

There are three important findings from the study: The uninsured rate is dropping, most people like their new insurance plans (even Republicans!), and most people are finding it easy to visit a doctor.

The study found the uninsured rate in the U.S. declined by one-quarter over the last nine months, which included the law's first, six-month open-enrollment period in which individuals could sign up for private insurance plans through exchanges established by the law.

From the July-to-September 2013 period to the April-to-June 2014 period, the uninsured rate of people between the ages of 19-64 dropped from 20% to 15%, according to the study. The research found 9.5 million people gained insurance, either through the exchanges or through the law's expansion of the federal Medicaid program.

The decline in uninsured was seen across different age groups and races, though the drop was disproportionately high among the young (-10%) and Latinos (-13%). It was disproportionately low among African-Americans — the decline was only 1%.

The findings show the law has been successful at reducing the uninsured rate among the poor — which was, of course, one of its main goals:

The Commonwealth Fund

Expectedly, there is a significant difference in the reduction of uninsured between states that have expanded Medicaid and those that have not. According to the study, the uninsured rate among residents who make up to 100% of the federal poverty level fell from 28% to 17% in the 25 states that have expanded Medicaid (plus the District of Columbia). In the 25 states that haven't, the rate only fell from 38% to 36%.

Among those who have become newly insured, the vast majority say they are "better off" and like their plans. In total, 58% of respondents with new plans said they are "better off" than before — including 61% who were previously uninsured. Seventy-nine percent of those who were previously uninsured said they were either "somewhat" or "very satisfied" with their new plans.

Even 74% of Republicans say they're at least somewhat satisfied with their new plans.

Significantly, most people who gained coverage under the Affordable Care Act said they couldn't have accessed care they have received since obtaining insurance:

The Commonwealth Fund

Finally: About one-fifth of people who have signed up for a new plan have attempted to find a new primary care or general doctor, and most — 75% — have said the process is at least "somewhat easy." Two-thirds of those who found a primary-care doctor got an appointment within two weeks. Thirty-seven percent of people said their new plans included "most" of the doctors they wanted (about 39% don't yet know).

The early days of the Obama administration were a chaos of uncertainty, between the historic housing bust, historic market crash, and historic armada of stimulus. But one thing was clear about the U.S. economy in 2008 going forward: Healthcare would keep on keeping on, in its insatiable way, adding more jobs, soaking up more tax dollars, and demanding a growing share of an American family's budget. In the worst recession in 80 years, it was the one industry that seemed truly recession-proof.

But these days, we're grappling with an interesting and opposite puzzle, one that is equally without precedent. The housing market is re-inflating, the stock market is up, and the stimulus has faded. But healthcare growth is—temporarily? permanently?—slowing down.

Before we get to the question marks, some context: In early 2009, healthcare employment had grown 22 percent since the day President George W. Bush took office in 2001. In that same time, overall employment had grown zero percent. Ze-ro. This discrepancy was among the more dramatic symptoms of growing healthcare costs. As debt piled up, Washington forecasters projected a not-so-distant future when Medicare, Medicaid, and Social Security would exceed all collected tax revenues. Even less lugubrious projections agreed that healthcare spending was just totally out of control, and this was even before some predicted that the Affordable Care Act (or, more commonly: Obamacare) would hasten the country's medical bankruptcy.

Meanwhile, five years after the passage of Obamacare, reality has intervened. Healthcare job growth fell throughout the Great Recession and has continued to fall, then stagnate, and then fall again. The labor market's runaway horse is clearly getting tired.

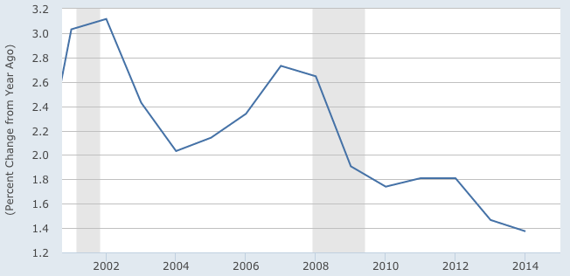

The deceleration of healthcare employment matches the slowdown in medical costs. After a roller-coaster ride through the last quarter of the 20th century, healthcare inflation looks like it's pumping the brakes to park near the 2 percent line, the lowest mark since the year Medicare and Medicaid were signed into law: 1965.

Growth in Medical Care Costs: Annual Percent Change

With slowly growing prices, even rising demand for healthcare has led to less-than-projected spending, in just about every category. (To be clear: This doesn't mean healthcare is getting cheaper; it means healthcare is getting more expensive slower than we anticipated.) The government is casually savinghundreds of billions of dollars in Medicare thanks to both direct cuts and other reforms. Insurance companies, despite a rough year due to the arrival of some expensive new drugs, have been spending less than the actuaries projected in 2010. Even with growth in high-deductible plans, out-of-pocket spending is actually coming in below projections from five years ago.

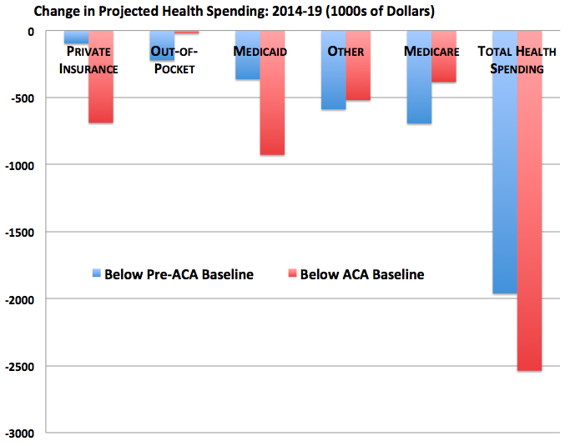

Forecasts of medical spending have undergone round after round of major surgery. Six years ago, the Urban Institute projected that the country would spend $23 trillion between 2014 and 2019. After Obamacare became law, it raised its forecast by half-a-trillion dollars. But the latest projections, published this month, are lighter by $2 trillion and $2.5 trillion, respectively.

Cheaper Than Advertised: Falling Healthcare Expenditures by Category

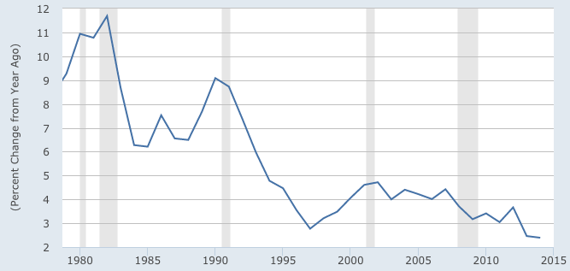

That leaves healthcare's $2 trillion question: What's going on exactly? Just about everybody agrees that the answer is "the recession and ..." followed by a smattering of variables, such as cost control measures in Obamacare, the rise of high-deductible plans, and reforms undertaken by doctors and insurance companies, independently, to curb over-treatment. It's strange to think that the recession, which technically ended in 2009, would still have its fingers around the neck of medical cost growth in 2015. But as you can see if you scroll back up to the second chart in this article, healthcare costs tend to follow the rest of the economy with a bit of a lag; prices were still decelerating years after the 1980s and 1990s recessions were over. There might even be signs that the slowdown is entering a new phase: Healthcare employment ticked up in the first quarter of 2015.

It's too early to predict how Obamacare will shape the U.S. healthcare system in the decades to come, especially given the upcoming Supreme Court decision. But as the U.S. enters the last quintile of Obama's term, the administration presides over a surprising historical moment. This was always going to be the Healthcare Presidency. But it wasn't obvious, even to the best actuarial oracles around, that the president who did the most to grow the government's role in healthcare since 1965 would preside over the period of slowest-growing healthcare spending since ... 1965.

01-15-2016, 11:13 AM (This post was last modified: 01-15-2016, 11:28 AM by admin.)

1) The reduction of the number of uninsured

Conservatives widely denied that the law would even succeed at its basic goal of increasing access to health insurance. Obamacare “created more uninsured people than it gave insurance to. And it promises to create even more,” argued National Review’s Jonah Goldberg. Fox News panelist Charles Krauthammer proclaimed the law would result in “essentially the same number of uninsured.”

Every serious method of measuring has shown the law effecting significant reductions in the uninsured rate. The latest, a report by the Urban Institute yesterday, shows that the uninsured rate has fallen nationally by 30 percent.

That's how many extra people with coverage? 16.3M people..

The number of uninsured persons continued to decline from 2013. In the first 6 months of 2015, 28.5 million persons of all ages (9.0%) were uninsured at the time of interview—7.5 million fewer persons than in 2014 and 16.3 million fewer than in 2013.

01-15-2016, 11:22 AM (This post was last modified: 01-15-2016, 11:24 AM by admin.)

2) Healthcare cost

In January 2010, the Congressional Budget Office projected that the federal health spending would total a bit more than $11 trillion between 2011 and 2020.

Today, the Congressional Budget Office thinks it made a mistake. Costs are coming in lower-than-expected, and the CBO's newest projectionssuggest the federal government will spend $600 billion less on health care than they predicted back in 2010.

So far, so good: projections are always wrong by at least a bit, and it's nice to have the extra $600 billion in America's pocket.

But here's the incredible thing: as Paul Van de Water, a health care expert at the Center on Budget and Policy Priorities, points out, the January 2010 projection didn't include any of the spending associated with Obamacare. The latest projections include all of the spending associated with Obamacare.

Reducing overall health-care costs. Obamacare actually had two different fiscal responsibility goals. The first was simply to offset the cost of new coverage with a combination of spending cuts and higher taxes — which, according to the Congressional Budget Office, it did. The second, more ambitious goal was to change the incentives that made doctors and hospitals eager to charge more money regardless of its effect, and that gave people who pay for that insurance little means to shop for better deals. Obamacare’s architects hoped that, on top of merely paying for the cost of new coverage, they could “bend the cost curve” downward.

When the law passed, conservatives insisted it would increase rather than decrease health-insurance costs. (Esteemed conservative intellectual Yuval Levin, in 2010, insisted it “completely fails” to reduce overall health-care spending.) Since the law passed, health-care inflation has fallen to historically low levels. Conservatives have repeatedly insisted this was a blip that would soon be reversed, and seized upon any apparent evidence for this case. When health-care spending spiked in the first quarter of 2014,Megan McArdle announced vindication: “After all the speculation that Obamacare might be bending the cost curve, we now know that so far, it isn’t.” (It turned out the first-quarter spike in health-care spending was a preliminary miscount that has since been corrected.)

Also yesterday, the Centers for Medicare and Medicaid reported that health inflation in 2013 not only remained in, it fell to the lowest level since the federal government began keeping track

Insurance competition. Obamacare is based on an old Republican plan, developed by the Heritage Foundation and first tried by Mitt Romney, whose central feature was market competition. The animating premise was that forcing insurance companies to lure customers on an open, regulated marketplace would bring prices down.

In all fairness, liberals did not place much faith in this dynamic. They didn’t accept a health-care plan that gave insurance companies a central role out of ideological conviction, but out of necessity — appeasing the industry, they calculated, offered them the only viable way to pass a bill through Congress. But the dynamic has turned out to work much better than expected. (The most natural ideological allies of the market function, conservatives, all committed themselves to the Republican Party’s totalistic opposition to every facet of the law.)

A surge in health insurer competition appears to be helping restrain premium increases in hundreds of counties next year, with prices dropping in many places where newcomers are offering the least expensive plans … In counties that are adding at least one insurer next year, premiums for the least expensive silver plan are rising 1 percent on average. Where the number of insurers is not changing, premiums are growing 7 percent on average.