I'll have a go at a few of the points being made:

1) Blaming the mess on predecessor

Well, you have to realize what happened in 2008 was really quite something else and produced a type of recession that is different from your garden variety business cycle, like the early 1980s, for instance.

It was caused by overleveraging, by households and banks, on the back of rising house prices. When the latter started to fall it destroyed household and bank balance sheets to such an extent that the bans had to be bailed out and households lost a whopping $9 trillion in wealth due to the 40% drop in house values.

The resulting deleveraging process means households borrowing and spending less, and saving more, paying off debt. This is indeed what happened.

Now, such a balance sheet recession is very different from the recession in the early 1980s:

- Reinhart and Rogoff have argued in a famous book based on historical data that these recessions take much more time to heal (and indeed, Japan spend a couple of decades deleveraging)

- Monetary policy is quite powerless as even at zero interest rates people prefer to pay off debt, rather than take on new loans

- There is a distinct danger of a Fisherian debt-deflationary spiral downwards without any policy intervention

- Fiscal policy becomes extra powerful because of the increase in savings produce low interest rates and there is plenty of spare capacity to avoid crowding out of the private sector.

The curious thing is, we know that monetary policy has been mostly exhausted and isn't very effective under such conditions, but fiscal policy is. Contrary to popular myth, the stimuls bill has been effective, just as austerity invariably produced bad results under these conditions, compare how the US fared with the US in 1937, or Japan in 1997, or Spain in the last two years. All cases are the aftermath of credit infused bubbles having imploded (that is, producing balance sheet recessions where the private sector pays off debt no matter how low interest rates go), but the latter three cases are where austerity was prematurely embarked upon, producing pretty disasterous results in the process.

Just this week, even the IMF has acknowledged this, arguing that fiscal multipliers are probably much larger than previously thought under these conditions (see post under Economy in this forum).

So what I take away from this is:

- Deleveraging is a lenghty process

- Fiscal policy is effectively the only tool when the private sector cuts borrowing and spending in order to repair balance sheets.

Where I respectfully disagree with conservatives is in their ridicule of the stimulus bill. Apart from being one of the largest tax cuts in US history(!), it has been rather effective to stem the verignious decline in 2008-9. This is what theory would predict under these circumstances, but also what happened on the ground. Economic growth, employment, world trade, world stockmarkets, they all fell with the same speed or even faster than in the early 1930s, until something arrested that decline..

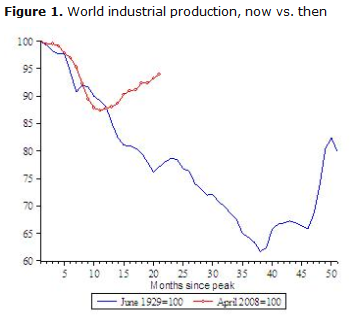

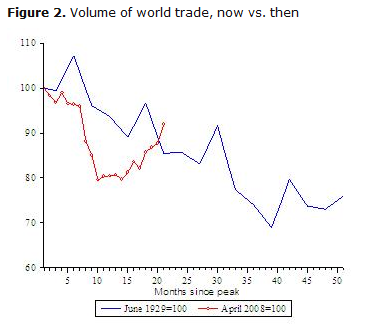

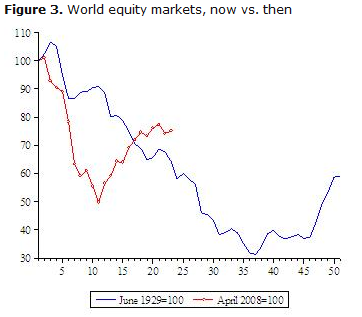

Here are Eichengreen and O'Rourke:

To sum up, globally we are tracking or doing even worse than the Great Depression, whether the metric is industrial production, exports or equity valuations. Focusing on the US causes one to minimise this alarming fact. The “Great Recession” label may turn out to be too optimistic. This is a depression-sized event.

A depression size event that didn't turn out to be a depression, let's keep that in mind..