The Shibor spike continues, this time with the Wall Street Journal:

The Chinese interbank funding market has seen rates soar since early this month amid slowing foreign-capital inflows and banks’ needs to fulfill investor obligations, among other factors. The squeeze is pushing up banks’ funding costs and could impede a key source of funds for growth even as the economy slows.

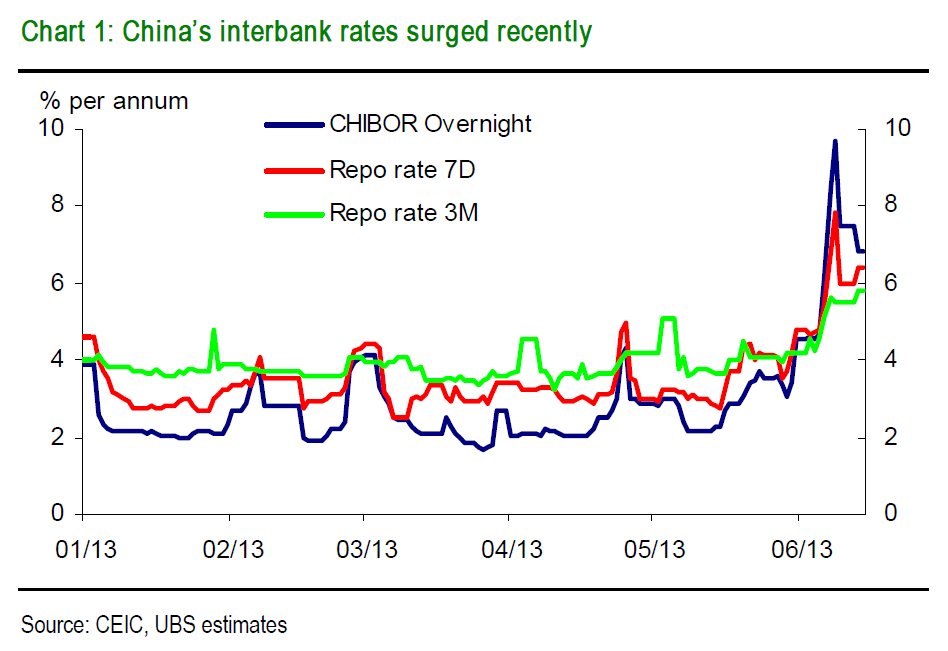

Originally, there were suggestions that the increase in China’s interbank interest rates was down to the Dragon Boat Festival holiday season and a resultant search for cash. But rates have stayed elevated as rumoured defaults and auction failures got everyone nervous and liquidity pressures mounted as foreign-capital inflows slowed and those dang wealth-management products demanded feeding.

In the larger picture, China’s current account surplus has fallen to 2.6 per cent in 2012 and, more narrowly, there was a significant drop in FX inflows in May.

UBS estimate that non-FDI net capital flows to China dropped from $40-50bn in March-April to $9bn in May. The official FX position at commercial banks, which includes FDI and current account flows, increased a mere RMB67bn in May, well short of the 300bn in April and 400bn a month in Q1.

Naturally, the banks are keen for the central bank to start spraying cash around, via a lower RRR, but there is a chance that this is actually more about the central bank looking to regain some control over the banks, and in particular unregulated bilateral lending between bank branches, rather than a serious cash squeeze.

And, well, intervention might look bad.

From the WSJ again:

Premier Li Keqiang, for instance, has indicated that Beijing is reluctant to change its monetary- and fiscal-policy stance to counter a slowdown while pledging to press ahead with changes that could make the country’s growth more sustainable.

“Right now, an RRR cut would be very controversial, because that would signal a change in macroeconomic policy,” said Li Wei, an economist with Standard Chartered in Shanghai…

A commentary published on Monday by China’s Financial Times, a newspaper backed by the PBOC, dismissed the prospect of a liquidity crisis in China’s money market but said some individual banks suffered funding problems because they had relied heavily on borrowing short-term funds in the interbank market and exceeded regulatory limits on lending. The article also said banks should sort out the funding problems on their own and shouldn’t count on the PBOC to step in to provide liquidity.

On Tuesday, the PBOC sold two billion yuan worth of 91-day bills the next day. The bill sale means that the central bank drained two billion yuan of liquidity from the money market, a negligible amount that would hardly sway the market but a signal China’s policy makers aren’t yet ready to loosen the grip on money supply

Anyway, here’s some analysts saying some relevant stuff (with our emphasis throughout).

First, Diana Choyleva at Lombard Street:

If the authorities decide to go for growth and engineer another stimulus, inflation is likely to rear its ugly head very quickly. The global financial crisis marked the end of the road for China’s export-led growth model. Unless there are structural reforms, just throwing money at the economy will produce inflation and bubbles rather than sustainable growth as happened after Beijing’s gigantic post-2008 stimulus. But this could well induce not just capital but also current account outflows.

Chinese households have two thirds of their financial wealth in interest-bearing deposits. Accelerating inflation hurts their real wealth. Moreover, last time around Beijing went for administrative control in its efforts to curb the overheating rather than raising interest rates and thus didn’t provide households with an offset. Accelerating inflation is also likely to drive domestic capital out. Moreover, a domestic stimulus in the face of still weak external demand is likely to further diminish the current account surplus if not turn it into deficit.

The other option is for the authorities to ease capital controls. Indeed, since the end of last year they have made concerted efforts to entice capital in by raising the foreign investor and offshore yuan quotas. In fact May saw the largest increase in the scheme that raises offshore yuan to invest in the mainland bond and equity markets since December 2012. The move was not just aimed at boosting the sagging domestic equity market, but also importantly to support bank liquidity. China’s banks may have been insolvent for a long time, but as long as they were liquid the excess investment show could go on.

The problem is that to place the economy on a sustainable growth path, China will have to open up outflows as well as inflows. Beijing made a more concrete commitment to allow Chinese people to invest abroad a few weeks ago. It will provide a concrete timetable by the end of this year. But if China opens up the capital account fully, outflows in search of higher return amid weaker and more volatile Chinese growth are likely to outweigh inflows.

Rising domestic liquidity pressures suggest that Beijing is likely to have to cut the banks’ required reserves ratio this year. At the same time, they could well raise domestic deposit rates as well which will be a necessary rebalancing measure until the market is allowed to set interest rates fully. Banks will bear the brunt of the structural adjustment China faces over the next few years. They will embark on a quest to raise capital abroad, but investors should be wary of the risks this will involve.

Then Anne-Stevenson Yang at j Capital:

We are all in an information vacuum. Clearly liquidity remains very tight even on Intervention Tuesday. We’re still two weeks out from Audit, so it seems unlikely this is temporary. I see it as part and parcel of the March moves to tighten up on irregular assets in the interbank market and I feel, without knowing for sure, that the mid-tier banks, the dodgiest of all, are in the crosshairs.

And finally, Tao Wang at UBS:

Banks have perhaps misjudged the PBC’s policy intension. With the economic data weak and disappointing and inflation low, many in the market had expected the PBC to ease monetary conditions more and some also anticipated a rate cut. However, the PBC seemed to be keen to keep a “prudent” policy stance and did not carry out reverse repos or initiate short-term liquidity operations as many expected last Thursday and Friday.

After the holiday ended on Thursday, the market was again surprised that the PBC chose to merely let the repos expire rather than actively injecting more liquidity to calm the situation. Feeling unsure about the central banks’ policy intention and perhaps also affected by external sentiment, banks have sought to increase their liquidity buffer, which has kept interbank liquidity tight and rates elevated.

Through the events over the past week, we think the PBC has made it clear that overly-rapid credit expansion would not be accommodated, and that the PBC still focuses more on the quantity of credit and money supply rather than on short-term interest rates. In other words, if banks let credit growth go too fast, the PBC does not mind the spike in interbank rates in order to rein them in. The recent episode may lead to banks trimming their credit exposure and manage liquidity more prudently henceforth, although there is a small risk that this could lead to a credit crunch in the short run. As such, we think the PBC will improve liquidity provision only gradually in the coming days and weeks, and do not expect any rate cut or reserve requirement cut. Behind all these is perhaps the central government’s increased tolerance for slower growth and increased attention to controlling financial risks.

UPDATE 1043 with more Wang thoughts, just sent through:

We think the PBC is right in trying to rein in credit growth and warn banks to properly consider liquidity and counter-party risks. We also think the regulators would be right in cracking down on reckless interbank- and other type of regulatory arbitrage through which banks increase leverage, hide loans, bad assets and risks. These actions would force banks to either increase risk weighting, which consumes more capital that they may not have, or more likely, bring some of the off-balance sheet credit onto the balance sheet and crowd out other loans. Managed well, such actions should lead to a gradual slowdown in credit expansion and a reduction in financial risks.

How much might credit be affected? For example, our bank analyst Irene Huang estimates that about RMB 2-3 trillion in bank credit may have been hidden in various interbank assets. If half of the credit were to be brought back to the balance sheet this year, this could lead to a drop in new credit by 1-1.5 trillion. As a comparison, total social financing (TSF) increased by almost 16 trillion in 2012 and 9 trillion in the first five months of 2013. In other words, with proper policy actions, China may well be able to keep TSF increase at about 16-17 trillion this year, which would mean keeping TSF growth at about 17-18% y/y, still sufficient to support a nominal GDP growth of 10% but slower than the 20% pace in 2012 and 22-23% pace so far.

But can this be managed smoothly or will it lead to a credit crunch and jeopardize this year’s growth, or worse, triggering a mini crisis? In our earlier research this year, we had pointed out that a high probability risk this year would be a liquidity crunch resulting from regulatory tightening or unstable funding in shadow banking.

We think the risk of a credit crunch has definitely increased over the past two weeks. While overall liquidity is still abundant, and the PBC still has a lot of tools to use if it deemed necessary, accidents could happen in the process of changing liquidity provision or cleaning up interbank activities. This is especially so when much of the credit expansion so far has been hidden off balance sheet and often under multiple layers of transactions, liquidity is unevenly distributed, and interbank transactions have made the system highly linked. Therefore, the central bank and other regulators must tread very carefully in the coming months in managing the process to try to minimize the risk of unexpected break in the liquidity chain or unwanted credit crunch.

Related links:

Swimming naked in China – FT Alphaville

China’s economy: new warning signs – Sober Look