Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

Early days, but this is the most important economic experiment of our times, it better succeed. There are other threads here explaining the Japanese predicament.

Japan current account surplus doubles as income gains, exports rise

Reuters – 43 minutes ago Reuters – 43 minutes ago

By Tetsushi Kajimoto and Kaori Kaneko

TOKYO (Reuters) - Japan's current account surplus doubled in April from a year earlier, and bank lending posted its biggest annual rise in over three years, in a fresh sign the government's aggressive policies to stimulate growth are paying early dividends.

Separate data showed the world's third-biggest economy grew 1.0 percent in the first quarter, revised up slightly from a preliminary estimate, underscoring a steady recovery driven by a pickup in global growth and sweeping stimulus policies by Prime Minister Shinzo Abe.

The current account surplus stood at 750 billion yen ($7.70 billion), up 100.8 percent from a year earlier and much bigger than a median market forecast of a 320 billion yen surplus, data from the Ministry of Finance showed on Monday.

Hefty income gains including returns from Japanese investments abroad, which were boosted by a weak yen, more than made up for trade deficits, analysts say.

"There isn't much change in the trade balance trend, where the weak yen is boosting import costs," said Junko Nishioka, chief economist at RBS Securities Japan.

"Exports are gradually recovering as overseas growth picks up, so that's a positive sign. But the growth in exports isn't strong enough to offset the rising import costs."

The latest data comes as volatile markets are casting a cloud over 'Abenomics', a policy prescription of sweeping monetary and fiscal expansion aimed at ending years of entrenched deflation and economic stagnation.

Japanese equities have suffered big falls since May 23, with investors worrying over a slowdown in China and uncertainty on when the U.S. Federal Reserve would roll back its stimulus.

The effects of a weak yen have had a bigger impact on boosting the cost of imports than driving export growth, posing a challenge to Abe's ambitious goal of putting Japan on a sustainable long-term growth track.

However, there are encouraging signals for the economy.

Bank lending rose 1.8 percent in May from a year earlier, the biggest annual increase since August 2009, in a sign the Bank of Japan's ultra-loose monetary policy is prompting companies to spend more.

For decades, Japan had accumulated solid current account surpluses, but the surplus for 2012 more than halved from a year before to 4.7 trillion yen, the smallest on record.

Separate data from the Cabinet Office showed Japan's economy grew 1.0 percent in January-March from the previous quarter, revised up from an initial estimate of a 0.9 percent gain due to revision to corporate capital spending.

Abe's growth strategy unveiled last week - 'the third arrow' of his three-pronged policies aimed at stimulating the Japanese economy - has so far failed to impress investors who want the prime minister to tackle bolder reforms including corporate tax cuts and higher labor mobility. ($1 = 97.3850 Japanese yen)

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

Krugman weighing in this morning:

Japan has announced a long-term turn to easier money and a higher inflation target. Stocks are up (if bouncing around a lot), the yen is down, but long-term interest rates are somewhat higher (although still very low). Is this a puzzle or a problem?

Richard Koo, Nick Rowe, and Noah Smith have all weighed in. So I guess I should put in my bit. Basically, I think Rowe is mostly right; Koo isn’t making sense; and Smith is worried for no good reason.

Let me start, as I often do, with my original 1998 itsy-bitsy liquidity trap model. This was an infinite-horizon model, but one in which all the action took place in either the first or the second period, since it was assumed that nothing would change after period 2. I imagined a situation in which a temporary negative shock to demand pushed the economy in period 1 up against the zero lower bound, and showed that in that case increasing the monetary base in period 1 had no effect. To get traction, the central bank would have to convince the public that it would increase the base in period 2 — e.g., that it would not withdraw any quantitative easing it was doing now — so as to generate expected inflation.

In that model, I only talked about the one-period-ahead interest rate. But we certainly could imagine two-period, three-period etc. bonds. How would an Abenomics-style monetary policy affect these longer-term rates?

Well, the answer would depend on what monetary policy is expected to do after period 2. If we’re looking at a one-time step up in the monetary base, which was my thought experiment in 1998, the short-term rate would remain at zero, and future interest rates would also remain unchanged, so no effect. But it’s easy to imagine that the change in monetary policy involves not just a one-time jump in the monetary base but faster growth forever after, or at least for a long time. In that case, future short-term rates will be higher in nominal (though not real) terms, and so long-term rates will rise even in period 1. The long rate will, however, rise by less than expected inflation, because the one-period-ahead nominal rate will stay at zero, so even as nominal rates rise, real rates will fall.

I think this is pretty much where Rowe is. Smith, however, loses the thread a bit, if I’m reading him correctly; he worries that the rising rates will cause a problem because of Japan’s huge public debt. But remember, while nominal rates may be going up, real rates are going down; so Japan’s debt becomes more, not less, sustainable. Also, bear in mind that there’s a lot of preexisting long-term nominal debt, whose real value will be eroded by inflation. So Abenomics is all good from a fiscal point of view, even if it makes headline interest payments rise.

Finally, Koo seems to regard higher inflation expectations as a disaster, when in reality they are the whole point of the exercise. What?

I guess I’ve always found Koo fairly incomprehensible on monetary policy. He emphasizes the importance of balance-sheet constraints, and deserves a lot of credit for being ahead of the pack here. He’s also right in emphasizing the useful role budget deficits can play in a balance-sheet recession. However, he has this violent opposition to monetary expansion that, as far as I can tell, isn’t actually justified — actually, isn’t at all justified — by his underlying analysis. On the contrary, when some of us (pdf) try to model Koo-type problems, we find that monetary policy that raises expected inflation could be quite helpful.

Maybe part of the problem is that Koo envisages an economy in which everyone is balance-sheet constrained, as opposed to one in which lots of people are balance-sheet constrained. I’d say that his vision makes no sense: where there are debtors, there must also be creditors, so there have to be at least some people who can respond to lower real interest rates even in a balance-sheet recession.

Also, if the problem is a debt overhang, isn’t debt-eroding inflation a good thing?

As I said, I just don’t understand Koo’s position here. If he wants to argue that monetary policy is unlikely to be effective, fine; but he wants to claim that it’s positively harmful, and I just don’t get the logic.

Anyway, back to Japanese interest rates: they really don’t pose a puzzle, nor, at least so far, do they pose a threat.

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

06-14-2013, 01:30 PM

(This post was last modified: 06-14-2013, 01:59 PM by admin.)

But there is also bad news out of Japan:

Nope not in that direction:

Up towards 18,000 in fact from it’s current bear-wrought 12,500 or so That’s Nomura’s bet at least and good luck to them A taste:

We have raised our end-2013 forecasts to 18,000 (previous forecast: 16,000) for the Nikkei Average and 1,500 (1,350) for the TOPIX, despite the market’s recent “new phase of declines” The assumptions on which our forecasts are based have changed from “little sign of recovery in earnings” and “expectations for Abenomics” to “earnings recovery” and “rise in global P/E ratios” We expect FY13 TOPIX-EPS to reach 82.5, surpassing its previous record high of 80 Japanese stocks are once again trading at lower P/E ratios than US stocks Assuming that Abenomics has not been defeated, we see no reason to become bearish on Japanese stocks, and recommend a bullish stance> We think the full impact of Abenomics on capex and household incomes has yet to be felt, which means that there are still substantial investment opportunities in these areas Our current recommendations are: (1) stocks generating strong earnings; and (2) stocks likely to benefit from the government’s growth strategies We reiterate our view that Japanese companies need to be extremely determined if they are to achieve new record highs for ROE

It is looking increasingly likely that the BOJ will take additional action now that the market environment has diverged from its initial expectations It is possible to conclude from this that the new phase of monetary easing is finally getting on course There appears to be something of a pause in the development of its growth strategies, but the Abe administration has responded quickly to market participants’ disapproval by revealing its intention to come up with further growth strategies, which we see as a positive The Upper House elections are scheduled for 21 July, and if the government looks likely to pursue its growth strategies, which constitute the “third arrow”, after the elections too, this should boost the stock market

A little more from Nomura’s note, which is the usual place The conflict between short term ‘fixes’ and longer term goals features prominently As it does in that chart near the top…

Abenomics revolves around steering Japan out of deflation via a combination of bold monetary policies, flexible fiscal policies, and growth strategies However, it faces a number of major obstacles; namely, (1) the markets regard a 2% inflation target as high, (2) the weaker yen has pushed up import prices but there has been only a limited improvement in incomes, and (3) long-term interest rates will have to be kept lower than nominal growth in order to avoid fuelling concerns about the government’s fiscal debt problems. We all remember situations when the stock market has been in turmoil and undergone a series of sharp declines because of concerns about how far long-term interest rates would be allowed to rise In this environment, it is difficult for Abenomics to stoke positive expectations

If share prices fall back to where they were before the BOJ announced its new phase of monetary easing (the 3 April Nikkei Average close of 12,36220), this could prompt market observers to pronounce Abenomics a failure The view that Abenomics has failed is likely to be accompanied by the opinion that the new phase of monetary easing has been unable to bring Japan out of deflation If Japan returns to square one despite this new phase of monetary easing, we think this will be a tragedy for the Japanese stock market Thus, Japanese stocks have been put in a very difficult position less than one month after the market’s sharp decline on 23 May Precisely because of this reason, we think the outlook for the Japanese stock market might vary quite substantially depending on whether or not share prices are able to remain at their current levels

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

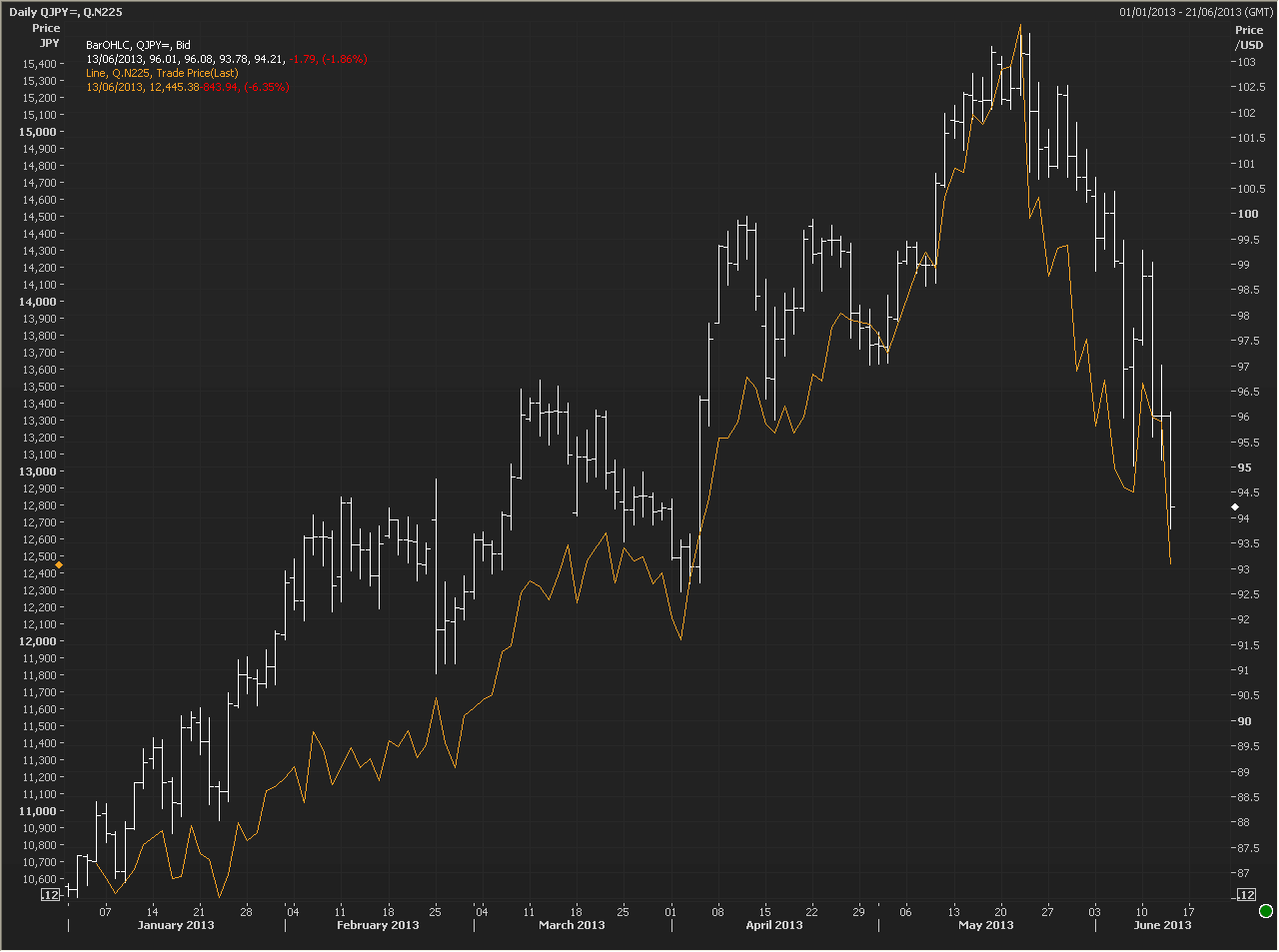

The Japanese stock market tumbled 6 percent in the most recent day of trading and has fallen by about 20 percent in three weeks. That comes on the heels of an enormous months-long rally touched off by Prime Minister Shinzo Abe's agenda of expansionary monetary policy. But it seems that what Abenomics giveth, Abenomics also taketh away.

One longtime Abenomics skeptic wagged at me when the Nikkei closed that this shows you can't achieve prosperity via currency debasement. But I think Lars Christensen's chart of inflation expectations reposted above shows the opposite. As long as investors believed that Abe and the Bank of Japan were committed to inflation, investors also believed in shares of Japanese companies. But rising inflation expectations pushed nominal bond yields up (as indeed they would almost have to), which sparked some highly public hand-wringing, a fall in inflation expectations, and a stock market crash. Some will see this as evidence that expectations-based monetary policy doesn't work (see Cardiff Garcia's useful roundup of fiscalists versus monetarists), but I tend to think that we're actually seeing the power of expectations. If BoJ President Kuroda were to issue a strong statement taking note of the situation and reiterating his intention to push inflation expectations back up to 2 percent despite being fully aware that this will increase nominal yields on Japanese bonds, then I bet that we'd see all these trends reverse.

But whatever you make of that, let there be no mistake—the Nikkei rally corresponded with a decline in the yen and a rise in inflation expectations while the crash has corresponded with a stronger yen and lower inflation expectations. The variable all move together. The scenario in which the currency is debased and the real economy suffers has not yet been seen.

Meanwhile in light of the continued debate on this topic, let me once again urge legislators in major developed countries to pass laws designed to explicitly authorize joint fiscal-monetary operations (i.e., "helicopter drops" in which, rather than purchasing bonds, central banks will directly give cash to citizens. The bond purchasing channel is problematic in a number of ways, not least of which is that it invites precisely the confusion over the direction of interest rates that seems to have tripped Japan up. When large-scale asset purchases push asset prices down rather than up, people become confused. Direct cash injections explicitly designed to boost prices and real output are clearer, fairer, and more transparent. in which, rather than purchasing bonds, central banks will directly give cash to citizens. The bond purchasing channel is problematic in a number of ways, not least of which is that it invites precisely the confusion over the direction of interest rates that seems to have tripped Japan up. When large-scale asset purchases push asset prices down rather than up, people become confused. Direct cash injections explicitly designed to boost prices and real output are clearer, fairer, and more transparent.

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

By Tatsuo Ito

The Bank of Japan's policy board has proven surprisingly united over the bold monetary easing program of its new governor, Haruhiko Kuroda. But there appear to be growing doubts over his goal to achieve a 2% inflation rate within the next two years to end years of deflationary pressures.

Mr. Kuroda managed to win a consensus within the nine-member board for his aggressive measures at his first meeting in early April. But there has been continued controversy over his insistence he can break 15 years of deflation and turn the current 0.4% annual fall in prices into a 2% rise.

Many private-sector economists who applaud the BOJ’s actions still contend the goal is unreachable, and such doubts have also emerged on Mr. Kuroda’s own board.

“It’s like they are all in the same boat but looking in different directions,” said one person familiar with the BOJ’s thinking.

The BOJ is increasingly confident about the near-term outlook for the economy and prices, people close to the central bank say. Japan’s GDP expanded at a 4.1% annual pace in the first quarter, the fastest among advanced economies. The consumer price index in the Tokyo metropolitan area, seen as a leading indicator for the nationwide trend, posted a gain in May for the first time in over four years.

The bullish view has done little, however, to narrow the differences over just how far and how fast prices can rise.

In an unusual move, board member Sayuri Shirai, a former economist at the International Monetary Fund, revealed her own figures for future price growth following the release of the central bank’s official outlook in April.

She said the year-on-year rate of change in the consumer price index will likely rise to around 1.0% for the fiscal year ending in March 2015 and slightly above 1.5% for the following year. The figures exclude the expected one-time impact from a sales-tax hike planned to begin in April 2014.

Those figures are lower than the nine-member’s board’s median forecast of a 1.4% rise for the year through March 2015 and 1.9% rise for the subsequent year. In a sign of how differently board members see the future, the projection for March 2016 ranged all the way from 0.8% to 2.3%.

Ms. Shirai’s comments added to the caution already expressed by her colleagues, Takahide Kiuchi and Takehiro Sato, former private-sector economists. The two openly disagreed with the forecast in April’s semi-annual outlook report that the CPI will likely reach 2.0% by the end of March 2016.

Other members, particularly Mr. Kuroda’s two deputies Kikuo Iwata and Hiroshi Nakaso and board member Ryuzo Miyao, have sided with the governor. They have stuck to the view that the BOJ must achieve the inflation target as quickly as possible to change a deflationary mindset that has become rooted among corporations and consumers.

Continue reading on Japan Real Time.

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

Well, the interesting experiment in Japan is continuing with some notable successes. GDP growth is up, prices seem to have stopped falling and are creeping up a little, this isn't surprising considering the acceleration in growth and the fall of the yen. There are some other things that are more problematic though:

- Some policy discord in the BoJ, although these are about future projections of inflation and therefore not terribly serious. However, considering the forces the BoJ faces (the volatility in the JGB market), the more united they are (or perceived to be), the better.

- Wild swings in stocks, currency, and bonds are in some way a measure of the BoJ discord.

- Disappointing program of the third arrow, structural reforms. But perhaps more will be forthcoming after the elections.

I would say, so far, so good, but the BoJ has to clean up it's act.

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

More good news out of Japan..

Reuters – 52 minutes ago

By Leika Kihara

TOKYO (Reuters) - Japanese manufacturers' sentiment turned positive in the three months to June for the first time in nearly two years, a closely-watched central bank survey is likely to show on Monday in a sign recent market turbulence has yet to hurt the feel-good mood created by the government's reflationary policies.

The Bank of Japan's "tankan" survey will likely show the headline index for big manufacturers' sentiment improved 11 points from three months ago to plus 3, according to a Reuters poll.

That would be the second straight quarter of improvement and the first positive reading - which means optimists outnumbered pessimists - since the survey of September 2011, and vindication of Prime Minister Shinzo Abe's "Abenomics" policy of aggressive monetary stimulus and fiscal spending.

Service-sector sentiment also likely brightened as consumers spent more, with the index for big non-manufacturing companies likely to have risen 5 points to plus 11, the Reuters poll showed.

A positive reading will bode well for the central bank, keen to end grinding deflation that has haunted Japan for 15 years and achieve its 2 percent inflation target in roughly two years through aggressive monetary stimulus.

"You cannot deny that the economy is improving, and that domestic demand is leading the way," said Hiroshi Miyazaki, senior economist at Mitsubishi UFJ Morgan Stanley Securities in Tokyo.

"Government stimulus spending is contributing to growth and the services sector is gaining strength. The BOJ's monetary easing is becoming more effective, so there's no need for additional measures."

The upbeat survey was compiled amid the market turmoil that drove up bond yields and wiped out gains in Tokyo shares made on hopes for Abe's stimulus plans. It should reinforce views the world's third-largest economy is steadily recovering, analysts say.

Big manufacturers and non-manufacturers both expect business conditions to improve further three months ahead, a sign they see the negative effect of the recent market turbulence on the economy as limited at least for now, the poll showed.

Positive market sentiment turned around in late May when the BOJ's huge asset purchases disrupted the bond market and drove up yields which, coupled with expectations of the U.S. Federal Reserve's tapering of monetary stimulus, hit global stocks and triggered a rebound in the safe-haven yen.

Still, the tankan report, a key touchstone for BOJ policymakers, will likely reinforce the view that Japan's economy remains on track for a steady recovery backed by a pickup in exports and private consumption.

The tankan's sentiment indexes are derived by subtracting the percentage of respondents who say conditions are poor from those who say they are good.

Big firms are likely to increase capital expenditure by 2.9 percent in the current business year from April, the Reuters poll showed, a sign the positive mood may be prompting them to expand business operations.

(Additional reporting by Stanley White; Editing by Eric Meijer)

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

The first bits of post-Abenomics data are finally trickling in. And so far, it has to be said, it’s looking good for Shinzo Abe.

Lombard Street Research’s Michael Taylor takes us through the initial findings (our emphasis):

A recovery in industrial production and consumer spending points to above-trend growth in Q2. Consumer price inflation may soon make a brief appearance above zero on the back of higher energy and import prices. But deflation isn’t beaten yet. The splurge of Japanese data overnight confirms the overall positive trend in the economy. Notably, industrial production increased by 2% in the month of May, the fourth consecutive monthly increase. Output in May was boosted by electronic components and machinery in particular. Both industrial production and exports are now on an upward trend (see chart below). To a large extent this recovery is due to the weaker yen. Although the yen is above its recent lows against the US dollar, it is still 19% lower than last November.

As for inflation and consumer spending:

As the chart (above right) shows, the fall in the yen has coincided with an equity market rally. This, plus an increase in inflation expectations triggered by aggressive monetary ease from the Bank of Japan, is also helping to boost consumer spending. For May household spending data show a 0.1% monthly gain, while retail trade data were up by 1.5%. Both are on an upward trend and will support another quarter of fairly robust GDP growth in Q2. Meanwhile headline CPI inflation was -0.3% in May, up from -0.7% in April.

Higher energy prices are contributing to less deflation. Electricity prices are up 8.7% over the last 12 months, the fastest rate in over 30 years. Higher import prices as a consequence of the weaker yen may push national CPI inflation slightly above zero in coming months. But of course this would not herald the end of deflation as underlying pressures remain deflationary.

Meanwhile, Nomura suggests that on the back of this data core inflation of positive 0.4 per cent might even be possible in June:

May core CPI, which excludes fresh foods, recorded +0.0% y-o-y, accelerating from -0.4% y-o-y in April. June Tokyo core CPI inched up to +0.2% y-o-y from +0.1% y-o-y. Partly thanks to a decline in prices from April to June last year, we think core CPI inflation is likely to rise further in June, recording positive inflation. Our economists think +0.4% core inflation in June is possible, the highest inflation since November 2008 (see “June all-Japan core CPI may come in at +0.4%”, 28 June 2013). Even though the expected spike in June comes partly from technical factors, +0.4% y-o-y inflation could positively influence inflation expectations.

Though, the lingering question remains, at what cost has all this come? And to what degree is it Japan that rumbled everything else in the market?

One chart worth reiterating on that front is the following, courtesy of Bond Vigilantes:

And as Reuters noted on Thursday:

Japanese investors’ net selling of foreign bonds hit its highest level in 14 months last week as they continued to defy expectations Japan’s radical monetary policy to reflate its economy would lead to a flight of investment out of the country.

Meaning very loosely that Japan’s gain is increasingly the rest of the world’s loss.

Related links:

Japan’s open goal – FT Alphaville

Females and the crisis – FT Alphaville

Everyone’s scared of something – FT Alphaville

Alphachat podcast: Noah Smith on the Japanese economy – FT Alphaville

|