Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

06-18-2013, 12:09 AM

(This post was last modified: 06-18-2013, 12:10 AM by admin.)

Fitch says China credit bubble unprecedented in modern world history

China's shadow banking system is out of control and under mounting stress as borrowers struggle to roll over short-term debts, Fitch Ratings has warned

The agency said the scale of credit was so extreme that the country would find it very hard to grow its way out of the excesses as in past episodes, implying tougher times ahead.

"The credit-driven growth model is clearly falling apart. This could feed into a massive over-capacity problem, and potentially into a Japanese-style deflation," said Charlene Chu, the agency's senior director in Beijing.

"There is no transparency in the shadow banking system, and systemic risk is rising. We have no idea who the borrowers are, who the lenders are, and what the quality of assets is, and this undermines signalling," she told The Daily Telegraph.

While the non-performing loan rate of the banks may look benign at just 1pc, this has become irrelevant as trusts, wealth-management funds, offshore vehicles and other forms of irregular lending make up over half of all new credit. "It means nothing if you can off-load any bad asset you want. A lot of the banking exposure to property is not booked as property," she said.

Concerns are rising after a string of upsets in Quingdao, Ordos, Jilin and elsewhere, in so-called trust products, a $1.4 trillion (£0.9 trillion) segment of the shadow banking system.

Bank Everbright defaulted on an interbank loan 10 days ago amid wild spikes in short-term "Shibor" borrowing rates, a sign that liquidity has suddenly dried up. "Typically stress starts in the periphery and moves to the core, and that is what we are already seeing with defaults in trust products," she said.

Fitch warned that wealth products worth $2 trillion of lending are in reality a "hidden second balance sheet" for banks, allowing them to circumvent loan curbs and dodge efforts by regulators to halt the excesses.

This niche is the epicentre of risk. Half the loans must be rolled over every three months, and another 25pc in less than six months. This has echoes of Northern Rock, Lehman Brothers and others that came to grief in the West on short-term liabilities when the wholesale capital markets froze.

Mrs Chu said the banks had been forced to park over $3 trillion in reserves at the central bank, giving them a "massive savings account that can be drawn down" in a crisis, but this may not be enough to avert trouble given the sheer scale of the lending boom.

Overall credit has jumped from $9 trillion to $23 trillion since the Lehman crisis. "They have replicated the entire US commercial banking system in five years," she said.

The ratio of credit to GDP has jumped by 75 percentage points to 200pc of GDP, compared to roughly 40 points in the US over five years leading up to the subprime bubble, or in Japan before the Nikkei bubble burst in 1990. "This is beyond anything we have ever seen before in a large economy. We don't know how this will play out. The next six months will be crucial," she said.

The agency downgraded China's long-term currency rating to AA- debt in April but still thinks the government can handle any banking crisis, however bad. "The Chinese state has a lot of firepower. It is very able and very willing to support the banking sector. The real question is what this means for growth, and therefore for social and political risk," said Mrs Chu.

"There is no way they can grow out of their asset problems as they did in the past. We think this will be very different from the banking crisis in the late 1990s. With credit at 200pc of GDP, the numerator is growing twice as fast as the denominator. You can't grow out of that."

The authorities have been trying to manage a soft-landing, deploying loan curbs and a high reserve ratio requirement (RRR) for banks to halt property speculation. The home price to income ratio has reached 16 to 18 in many cities, shutting workers out of the market. Shadow banking has plugged the gap for much of the last two years.

However, a new problem has emerged as the economic efficiency of credit collapses. The extra GDP growth generated by each extra yuan of loans has dropped from 0.85 to 0.15 over the last four years, a sign of exhaustion.

Wei Yao from Societe Generale says the debt service ratio of Chinese companies has reached 30pc of GDP – the typical threshold for financial crises -- and many will not be able to pay interest or repay principal. She warned that the country could be on the verge of a "Minsky Moment", when the debt pyramid collapses under its own weight. "The debt snowball is getting bigger and bigger, without contributing to real activity," she said.

The latest twist is sudden stress in the overnight lending markets. "We believe the series of policy tightening measures in the past three months have reached critical mass, such that deleveraging in the banking sector is happening. Liquidity tightening can be very damaging to a highly leveraged economy," said Zhiwei Zhang from Nomura.

"There is room to cut interest rates and the reserve ratio in the second half," wrote a front-page editorial today in China Securities Journal on Friday. The article is the first sign that the authorities are preparing to change tack, shifting to a looser stance after a drizzle of bad data over recent weeks.

The journal said total credit in China's financial system may be as high as 221pc of GDP, jumping almost eightfold over the last decade, and warned that companies will have to fork out $1 trillion in interest payments alone this year. "Chinese corporate debt burdens are much higher than those of other economies. Much of the liquidity is being used to repay debt and not to finance output," it said.

It also flagged worries over an exodus of hot money once the US Federal Reserve starts tightening. "China will face large-scale capital outflows if there is an exit from quantitative easing and the dollar strengthens," it wrote.

The journal said foreign withdrawals from Chinese equity funds were the highest since early 2008 in the week up to June 5, and withdrawals from Hong Kong funds were the most in a decade.

http://www.telegraph.co.uk/finance/china-business/10123507/Fitch-says-China-credit-bubble-unprecedented-in-modern-world-history.html

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

The Shibor spike continues, this time with the Wall Street Journal:

The Chinese interbank funding market has seen rates soar since early this month amid slowing foreign-capital inflows and banks’ needs to fulfill investor obligations, among other factors. The squeeze is pushing up banks’ funding costs and could impede a key source of funds for growth even as the economy slows.

Originally, there were suggestions that the increase in China’s interbank interest rates was down to the Dragon Boat Festival holiday season and a resultant search for cash. But rates have stayed elevated as rumoured defaults and auction failures got everyone nervous and liquidity pressures mounted as foreign-capital inflows slowed and those dang wealth-management products demanded feeding.

In the larger picture, China’s current account surplus has fallen to 2.6 per cent in 2012 and, more narrowly, there was a significant drop in FX inflows in May.

UBS estimate that non-FDI net capital flows to China dropped from $40-50bn in March-April to $9bn in May. The official FX position at commercial banks, which includes FDI and current account flows, increased a mere RMB67bn in May, well short of the 300bn in April and 400bn a month in Q1.

Naturally, the banks are keen for the central bank to start spraying cash around, via a lower RRR, but there is a chance that this is actually more about the central bank looking to regain some control over the banks, and in particular unregulated bilateral lending between bank branches, rather than a serious cash squeeze.

And, well, intervention might look bad.

From the WSJ again:

Premier Li Keqiang, for instance, has indicated that Beijing is reluctant to change its monetary- and fiscal-policy stance to counter a slowdown while pledging to press ahead with changes that could make the country’s growth more sustainable.

“Right now, an RRR cut would be very controversial, because that would signal a change in macroeconomic policy,” said Li Wei, an economist with Standard Chartered in Shanghai…

A commentary published on Monday by China’s Financial Times, a newspaper backed by the PBOC, dismissed the prospect of a liquidity crisis in China’s money market but said some individual banks suffered funding problems because they had relied heavily on borrowing short-term funds in the interbank market and exceeded regulatory limits on lending. The article also said banks should sort out the funding problems on their own and shouldn’t count on the PBOC to step in to provide liquidity.

On Tuesday, the PBOC sold two billion yuan worth of 91-day bills the next day. The bill sale means that the central bank drained two billion yuan of liquidity from the money market, a negligible amount that would hardly sway the market but a signal China’s policy makers aren’t yet ready to loosen the grip on money supply

Anyway, here’s some analysts saying some relevant stuff (with our emphasis throughout).

First, Diana Choyleva at Lombard Street:

If the authorities decide to go for growth and engineer another stimulus, inflation is likely to rear its ugly head very quickly. The global financial crisis marked the end of the road for China’s export-led growth model. Unless there are structural reforms, just throwing money at the economy will produce inflation and bubbles rather than sustainable growth as happened after Beijing’s gigantic post-2008 stimulus. But this could well induce not just capital but also current account outflows.

Chinese households have two thirds of their financial wealth in interest-bearing deposits. Accelerating inflation hurts their real wealth. Moreover, last time around Beijing went for administrative control in its efforts to curb the overheating rather than raising interest rates and thus didn’t provide households with an offset. Accelerating inflation is also likely to drive domestic capital out. Moreover, a domestic stimulus in the face of still weak external demand is likely to further diminish the current account surplus if not turn it into deficit.

The other option is for the authorities to ease capital controls. Indeed, since the end of last year they have made concerted efforts to entice capital in by raising the foreign investor and offshore yuan quotas. In fact May saw the largest increase in the scheme that raises offshore yuan to invest in the mainland bond and equity markets since December 2012. The move was not just aimed at boosting the sagging domestic equity market, but also importantly to support bank liquidity. China’s banks may have been insolvent for a long time, but as long as they were liquid the excess investment show could go on.

The problem is that to place the economy on a sustainable growth path, China will have to open up outflows as well as inflows. Beijing made a more concrete commitment to allow Chinese people to invest abroad a few weeks ago. It will provide a concrete timetable by the end of this year. But if China opens up the capital account fully, outflows in search of higher return amid weaker and more volatile Chinese growth are likely to outweigh inflows.

Rising domestic liquidity pressures suggest that Beijing is likely to have to cut the banks’ required reserves ratio this year. At the same time, they could well raise domestic deposit rates as well which will be a necessary rebalancing measure until the market is allowed to set interest rates fully. Banks will bear the brunt of the structural adjustment China faces over the next few years. They will embark on a quest to raise capital abroad, but investors should be wary of the risks this will involve.

Then Anne-Stevenson Yang at j Capital:

We are all in an information vacuum. Clearly liquidity remains very tight even on Intervention Tuesday. We’re still two weeks out from Audit, so it seems unlikely this is temporary. I see it as part and parcel of the March moves to tighten up on irregular assets in the interbank market and I feel, without knowing for sure, that the mid-tier banks, the dodgiest of all, are in the crosshairs.

And finally, Tao Wang at UBS:

Banks have perhaps misjudged the PBC’s policy intension. With the economic data weak and disappointing and inflation low, many in the market had expected the PBC to ease monetary conditions more and some also anticipated a rate cut. However, the PBC seemed to be keen to keep a “prudent” policy stance and did not carry out reverse repos or initiate short-term liquidity operations as many expected last Thursday and Friday.

After the holiday ended on Thursday, the market was again surprised that the PBC chose to merely let the repos expire rather than actively injecting more liquidity to calm the situation. Feeling unsure about the central banks’ policy intention and perhaps also affected by external sentiment, banks have sought to increase their liquidity buffer, which has kept interbank liquidity tight and rates elevated.

Through the events over the past week, we think the PBC has made it clear that overly-rapid credit expansion would not be accommodated, and that the PBC still focuses more on the quantity of credit and money supply rather than on short-term interest rates. In other words, if banks let credit growth go too fast, the PBC does not mind the spike in interbank rates in order to rein them in. The recent episode may lead to banks trimming their credit exposure and manage liquidity more prudently henceforth, although there is a small risk that this could lead to a credit crunch in the short run. As such, we think the PBC will improve liquidity provision only gradually in the coming days and weeks, and do not expect any rate cut or reserve requirement cut. Behind all these is perhaps the central government’s increased tolerance for slower growth and increased attention to controlling financial risks.

UPDATE 1043 with more Wang thoughts, just sent through:

We think the PBC is right in trying to rein in credit growth and warn banks to properly consider liquidity and counter-party risks. We also think the regulators would be right in cracking down on reckless interbank- and other type of regulatory arbitrage through which banks increase leverage, hide loans, bad assets and risks. These actions would force banks to either increase risk weighting, which consumes more capital that they may not have, or more likely, bring some of the off-balance sheet credit onto the balance sheet and crowd out other loans. Managed well, such actions should lead to a gradual slowdown in credit expansion and a reduction in financial risks.

How much might credit be affected? For example, our bank analyst Irene Huang estimates that about RMB 2-3 trillion in bank credit may have been hidden in various interbank assets. If half of the credit were to be brought back to the balance sheet this year, this could lead to a drop in new credit by 1-1.5 trillion. As a comparison, total social financing (TSF) increased by almost 16 trillion in 2012 and 9 trillion in the first five months of 2013. In other words, with proper policy actions, China may well be able to keep TSF increase at about 16-17 trillion this year, which would mean keeping TSF growth at about 17-18% y/y, still sufficient to support a nominal GDP growth of 10% but slower than the 20% pace in 2012 and 22-23% pace so far.

But can this be managed smoothly or will it lead to a credit crunch and jeopardize this year’s growth, or worse, triggering a mini crisis? In our earlier research this year, we had pointed out that a high probability risk this year would be a liquidity crunch resulting from regulatory tightening or unstable funding in shadow banking.

We think the risk of a credit crunch has definitely increased over the past two weeks. While overall liquidity is still abundant, and the PBC still has a lot of tools to use if it deemed necessary, accidents could happen in the process of changing liquidity provision or cleaning up interbank activities. This is especially so when much of the credit expansion so far has been hidden off balance sheet and often under multiple layers of transactions, liquidity is unevenly distributed, and interbank transactions have made the system highly linked. Therefore, the central bank and other regulators must tread very carefully in the coming months in managing the process to try to minimize the risk of unexpected break in the liquidity chain or unwanted credit crunch.

Related links:

Swimming naked in China – FT Alphaville

China’s economy: new warning signs – Sober Look

China's growth rate is slowing, yet debt levels are high and rising. We look at how the country got into this situation, and what it might mean.

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

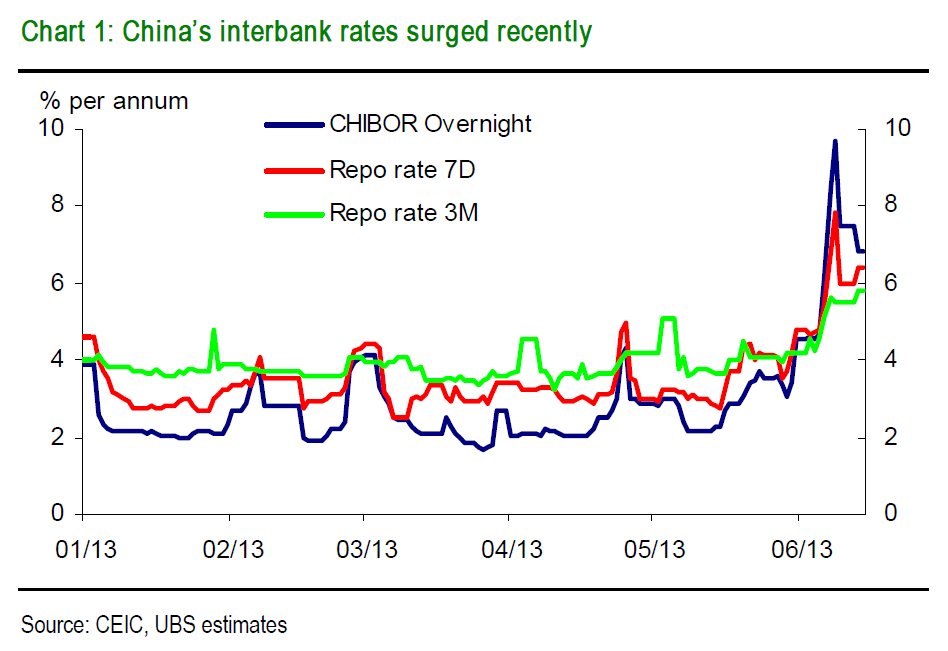

The headlines today were awash with relief that China’s liquidity crisis has subsided, as the central bank, the People’s Bank of China (PBOC), finally came to the aid of banks after a week-long standoff. But it’s hard to look at this chart and see cause for relief:

“Keep in mind 8-9% is right on the edge of the market breaking down,” says Patrick Chovanec, chief strategist at Silvercrest Asset Management. Even as the overnight rate came down, he notes, the 14-day and 1-month rates spiked today. “It’s kind of like how in Beijing…[the pollution has] been off the charts for so long that when it goes back down to ‘hazardous’ we’re like, ‘Oh, it’s great.’”

That’s because the core problem isn’t simply a seize-up in liquidity. Rather, it’s that rolling over the piles of debt amassed over the last few years requires ever-increasing amounts of liqudity, and that’s becoming harder and harder to perpetuate.

A debt crisis, not a liquidity crisis

“I think what people don’t really grasp is the extent to which this is not a liquidity crisis—it’s a debt crisis, so it’s not something that can go away,” says Anne Steveson-Yang, founder of Beijing-based J Capital Research. “They have a situation now where they’re running the whole economy on debt.”

What that means is that China’s massive stimulus from 2009 to 2011 sunk money into projects that are generating little or no returns. The continuing gush of credit allowed companies to paper over these losses by covering their bad debt with new loans. That combined with the fact that in the last two years, much of those loans haven’t appeared on bank balance sheets, and have instead been issued through shadow lending, has obscured the scale of China’s indebtedness. But whatever the size, it’s now big enough that the system needs colossal amounts of liquidity even to keep above water.

That $3.4 trillion in forex reserves? Irrelevant

So what can the Chinese government do about this? One thing the PBOC can’t do is use its foreign exchange reserves to bail out the banks. This is often assumed to be an option, but it isn’t. The PBOC’s $3.4 trillion in foreign exchange reserves are denominated in various currencies; selling them for yuan would strengthen the yuan, killing China’s export trade. It would also be massively deflationary, as it would reduce the amount of yuan in circulation. That would worsen the current liquidity squeeze unless balanced by a form of reverse sterilization, like lowering the required reserve ratio (RRR). And that brings us to the next point.

And slashing required reserve ratio…

The likeliest tool for increasing liquidity is lowering the required reserve ratio; this would allow banks access to more of their deposit bases. And they’re big—like, $3 trillion big. And many argue that, at around 75%, Chinese banks’ loan-to-deposit ratios are sufficiently healthy to make the move a safe one. By comparison, the US’s eight biggest banks had a combined loan-to-deposit ratio of 84% in Q4 of 2012. Here’s a look at the official data for all Chinese banks:

But this obscures the difference between big banks, whose ratio is somewhere around 70%, and the smaller ones, whose ratios are much higher than the average. That’s not exactly surprising. The big state-owned banks get to collect deposits, which they enjoy at government-set rates that many believe to be artificially low. In order to make money, the regional and commercial banks have to make more—and riskier—loans. And, sure enough, the proportion of loans that are bad is climbing (paywall).

And even assuming banks do have acceptable levels of outstanding lending, untold chunks of it are loans they’re never going to see again. As the Shibor shocks of this and last week suggested, smaller banks need constant fixes of cheap liquidity to prevent them from defaulting on loans. Though big banks are probably somewhat healthier, they’ve been raking it in off shadow lending, too.

…means more of the same

So the problem with lowering the RRR is that it would basically rev up the whole cycle of good credit chasing bad all over again. Those loans would also inevitably flow into the property market, driving already stratospheric prices still higher—a major policy worry for the central government right now. Plus, it would eventually gush back into the system, driving up prices for consumers.

In that sense calls for loosening kind of miss the point, as Silvercrest’s Chovanec points out. ”The PBOC isn’t taking away the punch bowl,” he says. “It’s refusing to go get a bigger and bigger punch bowl.”

So what’s on the horizon?

Even if it was unintentionally severe, the fact that the government has been crackdown on the interbank financing channels showed that government officials are intent on curbing excessive lending sooner. At the same time, a slew of wealth management products mature at the end of the June, which could trigger more interbank mayhem. That might be enough to prompt more loosening.

But even if the PBOC does pump money back into the system, it might not matter, says J Capital’s Stevenson-Yang, since big banks are too spooked to lend to smaller ones. “It will be calm now for a week or two and then there will be another shock—and a pretty big one,” she says. “It could be capital flight, or really bad trade numbers. But you’re going to hear the great sucking sound of money leaving China.”

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

FtAlphaville is the go-to place for China updates..

The PBOC’s “this is not the liquidity crisis you’re looking for” statement at the weekend may have drawn attention, but it didn’t really manage to reassure equity markets. The Shanghai Composite closed over 5 per cent lower on the day:

The issue at hand may be linked to this:

That would be the Chinese RMB weakening against the US dollar, in the context of a generally strengthening dollar index:

This is worth bearing in mind in light of the ‘other‘ hypothesis explaining some part of the trouble in China at the moment. This is based on the idea that the mother of all carry-trades may be being pushed to its limits by rising US bond yields, FX volatility and Fed taper speculation (if not the Chinese’ own attempt to stamp out over-invoicing practices).

Before getting to the general premise — some aspects of which seem to have been misunderstood by Free Exchange here — it’s worth outlining two potentially under appreciated points about China:

-

QE always ends up impacting China above all other countries due to legacy dynamics. In this way QE possibly represents more of a financial war with the PBOC (focused on finally appreciating the RMB vs the USD, or seeing the Chinese release its USTs) than explicit money printing in its own right. As Paul Krugman has said, contrary to what bond vigilantes believe, the US would in fact be a prime beneficiary of China releasing its USTs to the market.

-

To combat this, and to appear continuously in charge, China has been doing a fine PR job on the RMB, saying that it’s the one controlling the RMB appreciation path, it’s the one letting it trade in a larger band, and that it’s the one deciding that more foreign settlement should be allowed. As if these decisions are still theirs to make, rather than the obvious consequences of having to fight the QE valuation war, which has now led to a situation where the RMB may in fact be very much overvalued vs the dollar, rather than undervalued as many people still think it is. (Though this is very much a topic of hot debate.)

The other important thing to remember is that China’s role in world trade has been shifting significantly since 2008, as this chart from Societe Generale from May shows:

As the team noted in that context:

While between 2000-07 China’s exports rose at a faster pace than imports, by an average 2.5% per year; since 2008, imports are rising 4.5% faster pace than exports.

This is important because China has traditionally depended on FX purchases linked to its trade surplus to a) control the exchange rate and b) to distribute domestic liquidity into the system. When FX purchases dry up, so does the amount of RMB liquidity that’s distributed into the system which means the PBOC becomes dependent on alternative liquidity distribution mechanisms like repos, reserve ratio cuts and bill maturity.

The following chart from ChinaScope shows the degree to which the PBOC has been using repos to conduct its RMB-liquidity ops, and also — importantly — the degree to which central bank bills have been allowed to mature without compensatory issuance.

This is interesting given that China had witnessed six consecutive months of net foreign exchange purchases, suggesting the country was indeed benefiting from capital inflows. As noted here, however, the latest purchases resulted in a net increase of only 66.86 bn yuan, down some 77 per cent from April’s 294.35bn.

The smaller the net yuan injection, the less need for central bank bills to be issued. The greater the liquidity need, the more likely central bank bills are allowed to mature. What’s notable is that since July 2012 there has been very little net positive issuance of central bank bills, despite reserve ratio cuts, and that more recently bills have increasingly been allowed to mature on a net basis.

So how do we reconcile, a) the continuing FX inflows despite the shift in China’s role in world trade and b) the lack of bill issuance to mop up that extra liquidity?

Put another way, where did the FX used to create all that renminbi emanate from and where did the renminbi created by the FX purchase process end up?

One possible explanation is that a lot of the FX purchase were the result of borrowed dollars coming into the Chinese system, rather than pure trade dollars, and that much of the RMB liquidity created against those dollars headed straight into the weapons of mass ponzi market instead of Chinese Treasury bills.

If that’s true, a lot of what appeared to be a net capital inflow may have been an illusion, since the inflow was very much based on carry-trade fundamentals, facilitated by over-invoicing and other collateral-based trade finance shenanigans.

The Chinese government very publicly vowed to crack down on this sort of activity in May, but what’s worth asking is why did it choose to do so at that point? Was it because it genuinely wanted to lead a crack down on the practice, or was it because the government understood that the fundamentals sustaining the practice were likely unwinding in their own right and were soon to bring about nasty consequences that could make it look like the PBoC was losing control.

There’s no better PR management, after all, than making a bad thing look intentional and part of a deeper more considered strategy.

And if that’s true , one can imagine that the PBoC is delighted with everyone interpreting China’s current liquidity problem as being the intentional side-effect of a well-thought out government policy designed to stamp out shadow bank products — rather than the result of a wave of redemptions, brought on by the unwinding of the dollar-financing carry trade.

This also provides a useful explanation as to why the PBoC is not pandering to the sector’s demands for liquidity. And yet the truth may be linked to the fact that the PBoC cannot risk too much RMB liquidity being injected because this would have a detrimental effect on the USD/CNY exchange rate, and put pressure on the dollar shorts which created the surplus RMB in the first place.

And yet, the inability to meet RMB-denominated redemptions would lead to the same end result (dollar defaults) eventually anyway.

If that’s really what’s going on behind the scenes, then the only way to avoid dollar-financing pressure is for the Chinese government to begin liquidating (or repo-ing) some of its USTs so as to alleviate the dollar markets domestically.

In that sense, the Fed taper signal can also be seen as a message to China that it will no longer support cheap dollar financing in China, which is now delaying the inevitable moment that China release its USTs.

Very simplistically, the conclusion is: last year’s dollar shortage problem was potentially overcome by the opening of a major USD/CNY carry-trade which encouraged dollar borrowing. This was facilitated by the extension of QE. Furthermore, a lot of the net FX purchases of the last year were in fact fuelled by cheap dollar financing, rather than real trade surpluses — themselves synthetically pumped up on paper by fraudulent over-invoicing trends. This itself was encouraged by the out-of-this world returns which were being offered by the Chinese shadow bank market. All of which helped to support the yuan vs the dollar, and delay the inevitable moment that China was forced to liquidate or repo its UST hoards.

Unfortunately, Japan rumbled the whole balance by upsetting the UST demand balance in favour of JGBs — seeing UST yields rise — as well as adding volatility to the FX market, by strengthening the dollar against the yen, which led to Japanese exporters being favoured over Chinese ones.

If this has some bearing on reality — and at this stage most of this is indeed a theory — then one can expect either a spike in Chinese defaults (worsened, if RMB liquidity is dished out by the PBOC) and/or the liquidation of USTs. How likely that is depends entirely on how extensive the dollar-financing carry-trade really was.

If it really was more extensive than people realised, the only thing that can prevent either of the above scenarios playing out is the intensification of the carry-trade itself, or a genuine surge in China’s export business.

Yet, for the carry trade to continue to attract further capital and put off the dollar shortage problem, either the US has to continue to commit to easing, or the PBOC has to tighten enough to ensure that RMB returns domestically continue to more than compensate for the higher cost of USD funding, and that the RMB remains overvalued relative to the dollar.

It seems likely the Chinese government would prefer a genuine revival of Chinese exports. But it’s unclear how likely that is to happen in a world where China’s role in world trade has begun to shift from being a supplier of low-end manufacturing goods to the much more competitive area of value-added (hi-tech) products.

Related links:

Chinese ‘copper financing’ got even more popular this month – FT Alphaville

Is it policy? China edition – FT Alphaville

China’s two-way liquidity risk: capital outflows – FT Alphaville

The cheapest thing going is gone – The Economist

This is FT Alphaville's look at what degree of control China has over the shenanigans occurring in its interbank markets. Is this an exercise in domination by the PBoC or a demonstration of just how little sway it actually has?

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

Another excellent piece from FTAlphaville:

Should you panic?

It’s hard to know exactly what degree of control the PBoC has over the events unfolding in China’s interbank markets.

On the one hand, making the smaller banks and shadow finance entities sweat fits with the central bank’s new high-priority goal, introduced late last year, of containing ‘financial risks’, and also with a broader government theme of clamping down on excess.

On the other hand, Chinese liquidity is also being affected by external forces (shrinking capital inflows) and the shadow financing calendar (WMP end-of-quarter maturities). Michael Pettis says he suspects the PBoC was “caught flat-footed” by this combination of events, and it certainly isn’t hard to imagine. He also points out that this is a central bank which has almost no experience of any market conditions other than credit creation and expansion.

WMP redemptions could certainly be a problem this week. But WMPs have turned bad before, even affecting mid-sized banks in big cities, and their effect has been contained. That’s the (ahem) beauty of a command economy, in which banks and the media are under state control. Bank runs don’t spread so easily if people don’t hear about them.

Yet could this Chinese ability to conceal and contain financial panic be a double edged sword?

Pettis argues that for many years now, China has been able to use its opacity and control to boost its reputation for financial stability through low volatility. Those days may now be over (our emphasis):

Chinese financial markets often seem less volatile than one would expect for a poor, developing country, largely because of administrative measures that intentionally or unintentionally suppress normal volatility. These kinds of systems, however, are not less volatile. They seem less volatile because small shocks have minimal impact. Larger shocks, however, tend to cause a much greater than expected surge in volatility. Perhaps last week was a case in point.

Going forward we will probably see more of this in China. Volatility will be suppressed for periods of times only to erupt in greater than expected volatility from time to time. This is not only a China problem, of course. One can easily argue that the Fed’s actions under Alan Greenspan seemed to induce a “great moderation”, but only temporarily, and when the great moderation became less moderate, the economy was always likely to be more disorderly than expected. The euro, similarly, sharply reduced volatility in peripheral Europe for many years until it suddenly exacerbated it. Of course no student of Hyman Minsky would be surprised by any of this.

In fact, even suppressing bad news can backfire, he suggests. Pettis points to the panic in China over SARS early last decade as a possible case in point: although news of individual cases was often successfully damped down, rumours only grew and resulted in a panic that was arguably disproportionate to the outbreak. “(T)he attempt to suppress them can actually undermine credibility and so exacerbate the impact of the shock.” He writes that Argentina’s experience in 2001, when the government tried to deny it faced a payments crisis, is another situation where suppression of information may have made the resulting response even worse than if it had been admitted upfront.

Pettis, like StanChart’s Stephen Green, doesn’t think we are seeing a Lehman moment in China. But he does think there are three unanswered questions about this situation: if liquidity is adequate, as the PBoC says, where is it being hoarded?

Secondly, why hasn’t it received more attention from the mainland press (we think Pettis maybe answers his own question by wondering if it was an attempt to prevent depositor panic).

Thirdly, if there are large net redemptions from WMPs, where will that money show up? Writes Pettis:

I can only think of the following: more outflows from China, higher deposits in the banks, stock markets, real estate markets, cash hoarding.

None of which seem like particularly worthy destinations, if the PBoC is hoping its tactics will help improve the quality of credit allocation.

Again, the immediate facts prompt the question about how equipped the PBoC is to handle these situations, and whether the advantages it’s had in the past will continue to work at all, or even backfire.

Central banking is a confidence game. As Anne Stevenson-Yang of J Capital Research writes, the PBoC has to maintain the confidence of not just domestic financial participants; it also has to persuade speculative overseas capital that the country, and its currency, are still stable enough to invest in.

At the moment, the most likely end game of all of this is more realisation of misdirected investments that have resulted from the vast wave of credit growth over the past few years (which has in turn taken the place of export growth as China’s primary key of growth).

Recognising the misallocation — or being forced to recognise it — would in turn imply a steeper growth slowdown. Just look at how the sub-8 per cent growth has shaken global confidence. Nomura are now putting a 30 per cent chance of sub-7 per cent growth in H2.

Here’s another thought. Stevenson-Yang, who closely watches the amazingly rapid innovations in China’s shadow finance world, sees a risk that China’s feted huge foreign capital reserves could dry up.

That would be a shock.

Related links:

About those weapons of mass ponzi in China – FT Alphaville

This is FT Alphaville's look at what degree of control China has over the shenanigans occurring in its interbank markets. Is this an exercise in domination by the PBoC or a demonstration of just how little sway it actually has?

|