07-12-2015, 06:39 AM (This post was last modified: 07-22-2015, 08:57 AM by admin.)

Indicators measuring the overall regulatory environment show that Greece and Portugal are among the largest reformers: between 2008 and 2013, the two countries led the reform effort according to the OECD Product Market Regulation indicator.

The introduction of an electronic registry to simplify the creation of new businesses and the introduction of a new form of limited liability corporation that has no capital requirement may have helped Greece rise 110 places to 36th out of 189 in the World Bank’s Doing Business Report, the biggest improvement of any country between July 2012 and June 2013. There is also evidence to suggest that Greece’s efforts to liberalise its heavily protected professions have made some headway.

Data from the four countries confirms the large benefits of the EU’s Services Directive and the power of business environment reforms. Reforms implemented by mid-2013 are estimated to boost labour productivity in the sectors affected by the Directive by around 4.3 % in Portugal, 5.7 % in Spain, 7 % in Italy and almost 9 % in Greece. Given that the directive covers an average of 40 % of GDP in the four countries, the full economy-wide effects should be considerable.

An assessment of the liberalisation of 20 professions through the 2011 law by the Centre of Planning and Economic Research (KEPE, 2013) shows that the reforms liberalised professions substantially. The regulation index, which ranges from zero (no restriction) to 12 (maximum restrictions) declined on average from 5.8 before the reform to 2.3 after the reforms. As a result, 74 percent of the restrictions of the 20 professions were abolished. For non-scientific professions, the share went up to 83 percent. While regulations remained high for some professions, especially legal professions, the report argues that the remaining restrictions were broadly justified in view of the special nature of the services offered.

Anyone who opposes the prospect of a Grexit can feel a little lonely in Germany these days. Indignation over the Greek government is widespread and the seemingly endless rounds of debt talks have left the public drained. A Grexit seems to promise release and is looking increasingly appealing to many. But were Greece to leave the euro, the consequences would be disastrous -- for Europe, for Greece and indeed for Germany. It wouldn't be long before we would regret the day. Far more is at stake than just a few billion euros -- which are most likely already lost, anyway.

And for the Greeks, the insulting part of this proposal is that not only was their complete capitulation rejected, but the Eurogroup essentially blames Greece for getting in this position because of incompetence, writing: "There are serious concerns regarding the sustainability of Greek debt. This is due to the easing of policies during the last twelve months, which resulted in the recent deterioration in the domestic macroeconomic and financial environment."

some experts sharply observed that there probably isn't a plausible "time-out" scenario. Either Greece leaves the euro and its economy does fine, in which case Greece isn't likely to want to rejoin; or, Greece leaves the euro and its economy implodes, in which case the eurozone isn't likely to want Greece to rejoin the currency union.

What the German government is asking the Greek government to do about this is something that Germany rather infamously declines to do itself. In other words, they think the eurozone would be better off without Greece but they don't want to come out and say so. So they're piling-on demands, and hoping Greece turns them down.

So seems like the talk of Brussels has moved on to providing some form of bridging cash to keep Greece afloat until at least the summer when it faces a €7bn repayments schedule up until August. One suggestion doing the rounds is that Athens could now be given cash which was last reserved under the European Financial Stabilisation Mechanism(EFSM) first set up by the bloc as an emergency rescue fund in 2010. There's never a good time to discuss the differences between various euro rescue funds, and especially not in the early hours of the morning. But the important thing to note is that any cash under the original EFSM is likely to no longer be available for member states, as states by the eurozone's own treaties. According to the treaty which established the new permanent mechanism (ESM) and thus replaced its temporary predecessors: "the European Financial Stabilisation Mechanism (EFSM) will remain in force until June 2013. As this mechanism is designed to safeguard the financial stability of the euro area as a whole, the European Council agreed that Article 122(2) TFEU will no longer be needed for such purposes. Heads of State or Government therefore agreed that it should not be used for such purposes.

After 17 hours of tough negotiation, euro zone leaders have agreed a deal that could pace the way for a third Greek bailout. But it's far from a done deal. Here's a timeline of the key dates ahead as creditors prepare to dole out up to 86 billion euros ($95.2 billion) as part of a reform-for-aid package:

As the FT tells it, German Chancellor Angela Merkel and Greek Prime Minister Alexis Tsipras rose from their chairs at 6 a.m. on Monday and headed for the door, resigned to a Greek exit from the euro. "Sorry, but there is no way you are leaving this room," European Council president Donald Tusk reportedly said. And so a Grexit was avoided. But the FT's report is a bombshell, outlining just how hard the negotiations this weekend were for all involved. One participant described the negotiations as "violent." "They crucified Tsipras in there," one official told the FT.

Alexis Tsipras, Greece's prime minster reportedly asked for four concessions on the first draft. • No IMF involvement • A strong commitment on debt relief • A signal to the ECB to restart emergency loans • A smaller privatisation drive

The German government has just agreed, in principle, to another multibillion-euro bailout of Greece — the third so far. In return, it has received promises of economic reform from a Greek government that makes it clear that it profoundly disagrees with everything that it has just agreed to. The Syriza government will clearly do all it can to thwart the deal it has just signed. If that is a German victory, I would hate to see a defeat.

Meanwhile, ordinary Germans, Dutch, Finns and others also have every right to feel aggrieved. When they joined the euro, they were told that there was a “no bailout” clause in the treaty setting up the single currency. That was meant to reassure taxpayers that they would never have to pay the bills of other eurozone countries.

Assuming that the leaked deal is about right, and that it can be passed by the Greek parliament (and the loans approved by Germany, Finland etc), it seems more likely than not that we’ll see a sharp rebound in economic growth in Q4 of this year. These are my reasons for saying so

The agreement continues to require primary budget surpluses (net of interest payments), rising to 3.5% of GDP by 2018, which will worsen Greece’s slump. Re-profiling the country’s debt, which is implicitly part of the agreement, will do nothing to ameliorate this, given that interest payments already are minimal through the end of the decade. As the depression deepens, the deficit targets will be missed, triggering further spending cuts and accelerating the economy’s contraction.

Greece will need debt relief far beyond what euro zone partners have been prepared to consider due to the devastation of its economy and banks in the last two weeks, a confidential study by the International Monetary Fund seen by Reuters shows.

Another official close to the talks said the adjournment was prompted by a particularly heated exchange - on Greece's ability to service its debts - between European Central Bank chief Mario Draghi and German Finance Minister Wolfgang Schaeuble. In response to Draghi, one participant quoted Schaeuble as saying: "I'm not stupid." The veteran German conservative leads a hardline faction in the talks which warns Greece that it faces ejection from the 19-country euro zone if it does not do much more to earn its third bailout in five years.

Almost a million people, in a country of just over ten million, worked for the government in 2009. You could insist, as advocates of austerity have, that this was unsustainable, but throwing a third of those employees out of work, cutting remaining public-sector salaries by a third, and drastically reducing pensions, as advocates of austerity did, inevitably suppressed local demand.

The Israeli government’s decision to keep the new shekel constant and to seek free access to American and European markets was the foundation of the entrepreneurial economy that emerged in Israel during the nineties.

I noted last year that the assets of the Standard & Poor’s five hundred largest corporations were eighty-three per cent “tangible” in 1975, and eighty-three per cent “intangible” today. This means that production is now nested in what business managers call an “ecosystem,” which relies on shared science and large regional infrastructures, including stable currencies.

Just hours after a deal that saw Greece surrender much of its sovereignty to outside supervision in return for agreeing to talks on an 86 billion euro bailout, doubts were already emerging about whether Tsipras would be able to hold his government together. The terms imposed by international lenders led by Germany in all-night talks at an emergency summit obliged Tsipras to abandon promises of ending austerity. Instead he must pass legislation to cut pensions, increase value added tax, clamp down on collective bargaining agreements and put in place quasi-automatic spending constraints. In addition, he must set 50 billion euros of public sector assets aside to be sold off under the supervision of foreign lenders and get the whole package through parliament by Wednesday.

There has been an extensive discussion recently regarding the degree to which the limited access to financing facing Greek exporters imposes a constraint on their performance in international markets and, consequently, on the return of the economy to positive rates of growth. In the World Economic Forum’s report on competitiveness in the section entitled “the most problematic factors for doing business in Greece”, the limited access to financing of firms emerges as the second most problematic factor that has worsened due to the ongoing recession

Greece’s last-ditch bailout requires the country to sell 50 billion euros ($55 billion) of assets, an ambition it hasn’t come close to achieving under previous restructuring plans. The government of then-Prime Minister George Papandreou in 2011 set the same financial goal, which it sought to achieve by hawking airports, seaports, and beachside real estate. Since then, such deals have yielded 3.5 billion euros, according to the state privatization authority.

They could not go until they had reached a deal, he said. One official joked that he might have threatened to lock them in his office -- only he had no key. Merkel held her ground, anxious to keep the euro zone intact but conscious that many Germans, maybe including her own finance minister Wolfgang Schaeuble, would rather see Greece forced out. So too did Tsipras, pointing to estimates that companies on a list to be privatised may be worth only five billion euros. With the clock ticking, officials said it was Lagarde, with her IMF technical expertise, who broke the deadlock with a design for the fund that offered something for both sides.

So Greek exit from the euro would be hideous for banks. It would also be nightmarish for the European Central Bank (ECB). Here is one reason why. It currently holds €50bn of Greek loans to companies and residential mortgages - as part of the collateral on the €120bn of Emergency Liquidity Assistance it and the Bank of Greece have provided.

What happens if the IMF walks away you ask? Well, the entire "deal" could fall apart, as the Fund is expected to put up a not insignificant portion of the bailout money, and in the absence of that funding, the gap would have to be filled with "privitization proceeds" which the IMF itself has projected will come to just €2 billion over the next three years. Furthermore, German lawmakers, already exasperated with the protracted negotiations, would likely pull their support altogether.

In addition, an EU official said that of the €86bn in Greek financing requirements, the European Stability Mechanism — the eurozone’s €500bn bailout fund — was expected to put up only €40bn-€50bn. The current IMF programme, which still has €16.4bn in undisbursed funds and runs through March 2016, is expected to make up some of the difference, and eurozone officials had been assuming a follow-on IMF programme would contribute as well.

The IMF said the Europeans will either have to offer a “deep upfront haircut” or slash the debt burden by stretching maturities and presumably by lowering interest costs. “There would have to be a very dramatic extension with grace periods of, say, 30 years on the entire stock of European debt,” it said. Debt forgiveness alone would not be enough. There would also have to be “new assistance”, and perhaps “explicit annual transfers to the Greek budget”.

This is the worst nightmare of the northern creditor states. The term "Transfer Union" has been dirty in the German political debate ever since the debt crisis erupted in 2010. The underlying message of the report is that Greece is in such deep trouble that it cannot withstand further austerity cuts. This is hard to square with the latest demands by EMU creditors for pension cuts, tax rises, and fiscal tighting equal to 2pc of GDP by next year. Nobel economist Paul Krugman said the cuts are macro-economic "madness" in these circumstances.

As U.S. Treasury Secretary Jack Lew jets into Europe to urge policymakers to keep the Greek rescue on track, there are fears that the International Monetary Fund has derailed country's third bailout.

"If Germany wants the IMF on board it looks like it will have to give a lot more ground on debt relief or risk the agreement with Greece falling apart," Jasper Lawler, market analyst at CMC Markets said in a note Wednesday.

And Mr Varoufakis also assumed that the outside option for Greece was not all that bad. That means his hand, in a negotiation, would be very strong. That is because, quite recently, Greece was running a so-called "primary surplus" earlier this year. That means if it got cut off from financial markets because it failed to pay its debtors, it could still keep its public services running. I would presume he also thought the banks would be kept afloat by the European Central Bank: in previous chapters of the crisis, it actually rewrote its own rules to keep the banks open and liquid in Greece. In that situation, Mr Varoufakis thought the damage would be much worse to Europe than it would be to Greece of a failure to agree.

one person who has read it is the former finance minister Yanis Varoufakis. And not only that: just hours before what may be the most critical vote in Greek history, he has released an annotated version of what the Euro Summit statement really means for Greece.

It's about time Greece left the euro — it's the only way to keep the country from falling further into the black hole of debt that is ravaging its economy. Greece has too much debt. In fact, it's "highly unsustainable" according to the International Monetary Fund, and the only way the country will remotely have a chance of getting this reduced is by a Greek exit from the euro, or Grexit.

The IMF isn’t a creditor in the usual sense of the word. It’s a collateralised bilateral swap agent that exists to help countries balance international payment obligations so that they don’t have to start wars, grab resources or asset-strip trade partners when they abuse their trust. The clue comes in the ‘F’ of the IMF acronym, which of course stands for fund not force. But even that is a misdirection, since the fund is actually made up of capital commitment quotas, not pre-paid lump sums of capital. Pre-paying would be dumb, you see — a waste of perfectly good capital. What if there’s no crisis to allocate the funds to? That capital just goes to waste, unused. What the quotas really are then are capital pledges. This loosely translates to signed up IMF members agreeing to freeze their own potential counter claims on trade partners who can’t afford to balance their IMF account, until the country in question can afford to honour them. In the event the “creditor” nations don’t have counter claims, they simply agree to assign claims on their own capital resources, and so forth, in exchange for eventual claims on the country in question. That’s why you can’t actually technically default. It’s not a loan. It’s a swap.

Greece's third bailout agreement in five years was passed by the country's Parliament earlier this week, despite a national referendum that rejected new austerity measures. The resulting collapse of Prime Minister Alexis Tsipras' Syriza-led coalition and the protests that erupted in Athens showed that many in Greece are still asking themselves whether the ultimate prize — continued euro membership — is worth the pain of more austerity. History might have some answers.

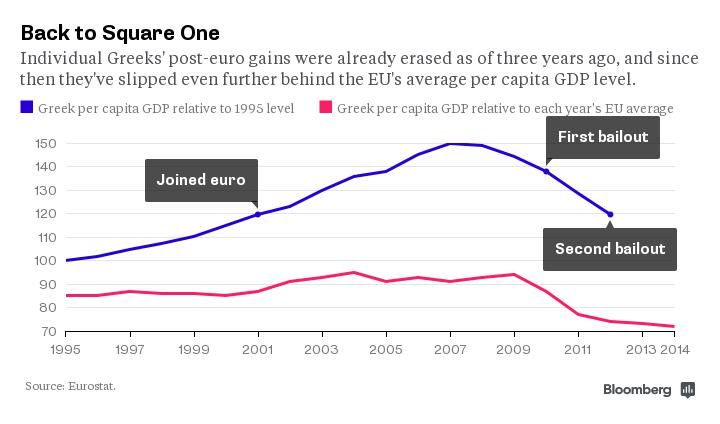

1. GDP per capita

Membership in the single currency was initially great for the Greeks. The size of their economy (on a per person basis) rose by 25 percent, and came very close to reaching the European Union average. Then Greeks watched in horror as the global recession and later their own debt crisis erased all those gains in just a few short years. By 2012, Greeks' per capita share of real GDP was the same as in 2001 and had fallen to 74 percent of the EU average.

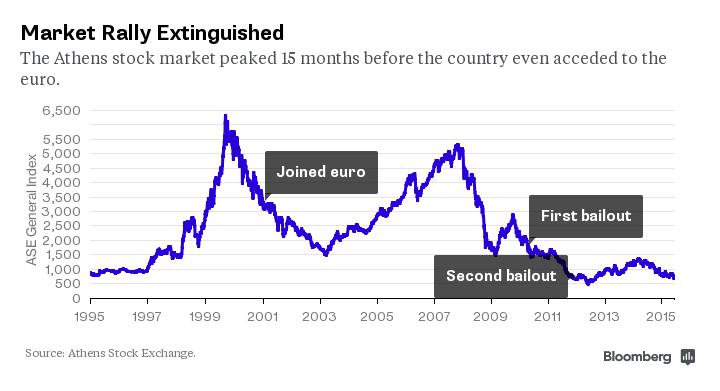

2. The stock market

If we take the Athens Stock Exchange as a proxy for the corporate sector, it's even harder to see the euro's benefits to Greece's companies. While there was a prolonged recovery in the market between 2003 and 2007, the main index never returned to its pre-euro record level of 6,355 and has since fallen to below 800.

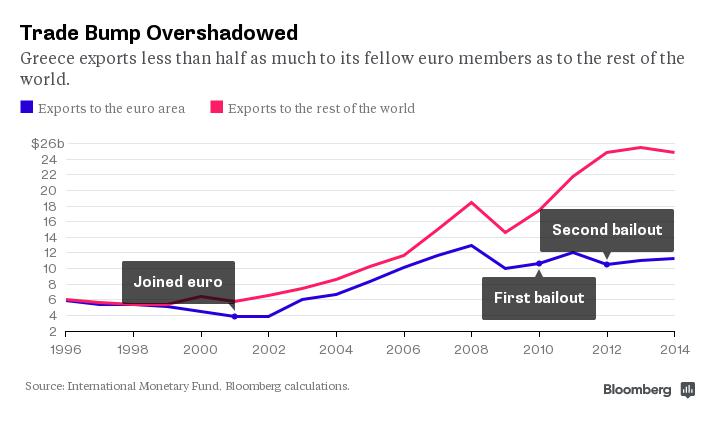

3. Trade

One positive benefit you'd certainly expect to accrue to Greece from joining the euro is a big surge in how much trade it conducts with the countries it now shares a currency with. That's exactly what happened. Compared to $4.5 billion in Greek exports to euro-area countries in 2000, before it joined, that figure rose to $11.2 billion in 2014. The only wrinkle is that over the same period Greece increased its exports to non-euro countries by even more, from around $6.5 billion to nearly $24.8 billion, undermining a key argument in favor of creating a currency union in the first place.

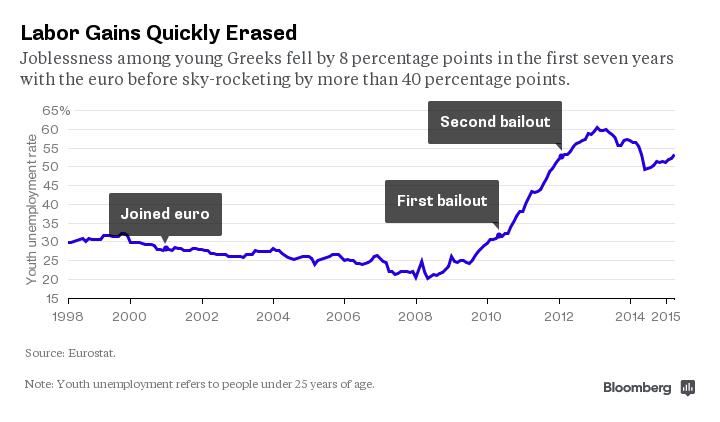

4. Jobless youth

Turning to the labor market, it should be noted that the unemployment rate was already falling by the time Greece joined the euro. Still, the first few years in the single currency zone saw fewer and fewer Greeks out of work, with an especially impressive drop in the country's unemployment rate among 15 to 24 year-olds. That was particularly good news for an economy that has long sidelined far too many of its willing and able young workers. With the global recession and the continuing debt turmoil, that progress has long since evaporated. Youth unemployment is now above 50 percent, the second highest rate globally, according to the World Bank.

5. Savings

Lastly, while Greeks had maintained savings worth over 16 percent of national GDP for much of the late 1990s, access to increasingly cheaper credit facilitated a multi-year spending spree. The savings rate then plummeted to as low as 4 percent. Now that the cheap credit is gone and a long recession has made consumers more conservative, Greeks are once again squirreling away money. By 2013 the country had the equivalent of nearly 11 percent of GDP saved up. It's not enough to pay off the government's crippling debt, but it's a start.

The slow recovery from the crisis of the euro zone as a whole is the result, among other factors, of (1) political resistance that delayed by many years the implementation of sufficiently aggressive monetary policies by the European Central Bank; (2) excessively tight fiscal policies, especially in countries like Germany that have some amount of "fiscal space" and thus no immediate need to tighten their belts; and (3) delays in taking the necessary steps, analogous to the banking "stress tests" in the United States in the spring of 2009, to restore confidence in the banking system. I would not, by the way, put "structural rigidities" very high on this list. Structural reforms are important for long-run growth, but cost-saving measures are less relevant when many workers are already idle; moreover, structural problems have existed in Europe for a long time and so can't explain recent declines in performance.

As I discussed in an earlier post, Germany has benefited from having a currency, the euro, with an international value that is significantly weaker than a hypothetical German-only currency would be. Germany's membership in the euro area has thus proved a major boost to German exports, relative to what they would be with an independent currency. Nobody is suggesting that the well-known efficiency and quality of German production are anything other than good things, or that German firms should not strive to compete in export markets. What is a problem, however, is that Germany has effectively chosen to rely on foreign rather than domestic demand to ensure full employment at home, as shown in its extraordinarily large and persistent trade surplus, currently almost 7.5 percent of the country's GDP.

The euro might be worse for you than bankruptcy. That, at least, has been the case for Finland and the Netherlands, which have actually grown less than Iceland has since 2007. Iceland, you might recall, went bankrupt in 2008. Now, it's true that Finland and the Netherlands have had their fair share of economic problems, but those should have been manageable. Neither country is a basket case, and both have done what they were supposed to do. In other words, they've followed the rules, and the results have still been a catastrophe. That's because the euro itself is. Or, if you want to be polite, the common currency is "imperfect, and being imperfect is fragile, vulnerable, and doesn't deliver all the benefits it could." That was European Central Bank chief Mario Draghi's verdict on Thursday.

The International Monetary Fund's July 14 forecast for Greece's debt as a share of gross domestic product in 2017 was almost 200 percent, up substantially from its April estimate of 151.8 percent.

Nevertheless, perhaps it is the right time to look back and reflect on the experience of Greece and other countries who have implemented rescue programs and reformed their economies in distress to draw lessons. These may help in future policy choices. Below I offer five but it is not a complete list.