Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

Then there is this:

-

Total U.S. athletic footwear point-of-sales rose 10.7% Y/Y for the week ending December 12, according to data from Sportscan.

-

Unit sales were up 5.7%, while the average selling price increased 4.7% during the week. Both marks easily top growth rates across broad retail.

-

Sales in the basketball category were up 20% from the corresponding week a year ago. Nike (NYSE:NKE), Adidas (OTCQX:ADDYY), and Under Armour (NYSE:UA) are the dominate basketball players, while Foot Locker (NYSE:FL) and Finish Line (NASDAQ:FINL) are thriving selling channels. On a side note, Finish Line's website was queuing visitors this morning due to heavy traffic.

-

The casual athletic footwear category was up even hotter than basketball with a 32% pop. Wolverine Worldwide (NYSE:WWW) and Skechers (NYSE:SKX) are likely to have scored a lot of that action. Nike's Converse brand is also a major force in casual athletic. Sales of the iconic Chuck Taylor line have almost doubled over the last five years to top $2B.

-

Running shoes sales increased 7.6% during the key week.

-

Sector leader Nike reports earnings on December 22. A strong read on futures orders could resonate across the industry.

-

Previously: Confidence in Nike ahead of earnings week (Dec. 18)

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

01-06-2016, 09:52 AM

(This post was last modified: 01-06-2016, 09:52 AM by admin.)

Footwear retail stocks, such as Foot Locker and Finish Line, have come under pressure recently due to ongoing concerns of a slowdown in athletic footwear and basketball shoes sales. In a report published Friday, Paul Trussell of Deutsche Bank argued that concerns over a slowdown are overblown. The analyst acknowledged that while an increased emphasis on DTC (direct to consumer) by vendor partners, heightened inventories and poor results from Skechers USA Inc (NYSE: SKX) are all valid concerns and "warranted," they are "not new." Trussell continued that athletic footwear sales have been "robust," given their overall mid-single digit growth over the past few years. In fact, total athletic footwear sales are higher by 5.7 percent year-over-year for the last 13 weeks and up 6.9 percent year-to-date – an improvement from the 2.8 percent growth the segment saw in 2014.

Deutsche Bank Sees 'Solid' Overall Athletic Footwear Sales - Yahoo Finance

That increased emphasis on DTC is interesting, for instance at Nike:

Nike (NKE) comes ahead of direct-to-channel sales projections

Nike (NKE) plans to grow its direct-to-consumer, or DTC, sales almost 2.5x in the next five years, from $6.6 billion in fiscal 2015, to $16 billion by fiscal 2020. The company beat its own target of $5 billion in DTC sales by fiscal 2015, announced at its last investor day in 2013, by over $1.5 billion.

DTC sales include sales made through the company’s own stores, both factory and in-line, and through nike.com. These channels key drivers of sales for the brand overall. Nike’s company-owned stores, particularly brand statements like the NikeTowns in New York and London, it addition to Nike’s websites, enable Nike to market the brand effectively, thus driving sales across channels, geographies, and categories.

Web sales guidance

Nike.com is expected to be a key driver for DTC sales, with $7 billion in e-commerce sales expected by fiscal 2020.

Online sales came in at ~$1.2 billion in fiscal 2015. That would take the e-commerce contribution to 14% of sales in fiscal 2020, up from ~3.9% in fiscal 2015.

Global rival Adidas (ADDYY) is targeting over 2 billion euros from web sales by 2020, as detailed in its latest five-year plan unveiled in March 2015. Under Armour (UA) hopes to grow its web sales five-fold by 2018, though it didn’t provide a sales figure at its 2015 Investor Day.

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

Skechers' sales are soaring. The company's revenue in fiscal 2015 totaled $3.15 billion, which represents a 32% gain over the previous year. Skechers' recent success can be attributed in part to consumers' growing preferences for comfortable, stylish shoes over basketball sneakers, according to a new report from Morgan Stanley.

Skechers poised for growth - Business Insider

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

The company expects to open 200 new stores by the end of 2016, the shift away from wholesale also helped in boosting its gross profit. It is expanding internationally at a fast clip, with second quarter sales at its stores abroad rising by 40% from the year before. While domestic wholesale sales fell by 5.4% in the quarter from a year ago, company-owned retail-store sales grew by 15%. .. At the end of the quarter the company had 546 company-owned Skechers retail stores, of which 142 are outside the US. Skechers opened an additional 23 retail stores this quarter.

Skechers USA, Inc. - International Growth Will Propel The Stock Higher - Skechers USA Inc. (NYSE:SKX) | Seeking Alpha

Also, with the stock setting 52 week low prices, insider buying would be appropriate if there is a worthwhile opportunity. However, an online Form 4 screener merely shows fervent selling. The CEO, Robert Greenberg, is incentivized to drive the share price higher because he owns 45.0% of outstanding Class B common shares, and members of his immediate family own an additional 15.7%. Further, Gil Schwartzberg, trustee of several trusts formed by Mr. Greenberg and his wife for estate planning purposes, beneficially owns 38.7% of outstanding Class B common shares. As a result, open market insider buying by them would be a surprise (Source 10K).

Skechers: Underperformance, Global Acceleration And Pressured Margins - Skechers USA Inc. (NYSE:SKX) | Seeking Alpha

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

Without a doubt, Skechers has had an incredible 3 years with sales projected to double this year from 2013 levels and earnings to be up nearly 6 fold from 2013 levels. That rate of growth is clearly unsustainable, but it does evidence the fact that Skechers is a completely transformed company from several years ago. We still think public perception is poor in Skechers and hence the steeply discounted valuation. Okay, so as we stand today, Skechers is selling at a massive discount to its competitors, but what is the forward-looking prognosis for the company?

The last 3 years of rapid sales and earnings growth and free cash flow have put Skechers on a very solid financial path. The company has spent $200 million to build out retail stores and build US and global distribution capabilities. Even with that, the company has $620 million in cash and $60 million of long-term debt. By year end, we project the company to have $750 million in cash and approximate annual free cash flow of $250 million per year. That's pretty amazing for a company with a market capitalization of only $3.7 billion.

Skechers Valuation: As Cheap As It Gets - Skechers USA Inc. (NYSE:SKX) | Seeking Alpha

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

There is obviously a model shift happening at skechers. Thru q2 2016, domestic wholesale business is up 2%, international wholesale is up 40% and company owned retail is up 18%. Selling thru US department store chains is pretty stagnant, the good news of that is that the domestic wholesale channel is the lowest gross margin of their 3 divisions at 37%. Company owned retail gross margin is 60%(no middle man) and international wholesale at about 43%. China margins are probably in the 45% range.

Skechers Valuation: As Cheap As It Gets - Skechers USA Inc. (NYSE:SKX) | Seeking Alpha

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

Selloff on downgrade:

Morgan Stanley’s Jay Sole pointed out that the shift in consumer preference to pure fashion footwear is pushing Skechers USA Inc SKX 8.29% to adjust its assortment, leading to slower-than-anticipated sales growth and SG&A deleverage. Sole downgraded the rating on the company from Overweight to Equal Weight, while lowering the price target from $41 to $25... Skechers needs to spend more than earlier expected to add distribution capacity in Europe, South America, China and the United States. An additional $75–$100 million is required for corporate office space improvement. “We see no positive fashion catalysts until 1H17 and expect Street EPS estimates to fall over that time frame. However, with the stock trading at just 12.5x our new FY17 EPS estimate, we think some of this bad news is priced in,” Sole explained. The FY17 EPS estimate has been lowered from $2.25 to $1.85 to reflect order delay and increased SG&A.

Morgan Stanley On Skechers: 'Three Stripes, You're Out' | Benzinga

Bad news priced in, that seems an understatement to us.. And not all analysts are as negative as Morgan Stanley:

While there have been concerns surrounding the athletic apparel and footwear trend, Skechers USA Inc SKX 8.39% has more than a 20 percent growth opportunity over the next two years, Citi’s Scott T Chronert said in a report. He maintained a Buy rating on the company, while adding the stock to the SMID Value Creators Focus List. Although the athletic apparel and footwear trend seems to be “in the later innings,” Skechers’ global growth prospects remain intact, analyst Chronert commented. The company is likely to deliver a positive earnings inflection in H2, following a y/y decline in comps in Q2... Although there is risk related to Skechers’ Q3 results being impacted by “some lingering promotional activity,” this is already reflected in the company’s current valuation and trading patterns, the analyst noted. Overall Strength “We have increased confidence in Skechers’ international momentum, its strong balance sheet and clean inventories,” Chronert wrote. Since the company faces easier comps in H2, the recent pressure on shares “could prove to be an attractive entry point.”

Skechers U.S.A., Inc. (NYSE:SKX) - Skechers A Top Opportunity, Says Citi | Benzinga

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

SKX has been the topic of several other research reports. B. Riley reiterated a buy rating and set a $42.00 price objective on shares of Skechers USA in a research note on Tuesday, July 19th. Monness Crespi & Hardt lowered shares of Skechers USA from a buy rating to a neutral rating in a research note on Friday, July 22nd. They noted that the move was a valuation call. Zacks Investment Research upgraded shares of Skechers USA from a sell rating to a hold rating in a research note on Monday, July 18th. Susquehanna initiated coverage on shares of Skechers USA in a research note on Friday, August 12th. They set a neutral rating and a $27.00 price objective on the stock. Finally, Argus lowered shares of Skechers USA from a buy rating to a hold rating in a research note on Monday, August 1st. Eight equities research analysts have rated the stock with a hold rating and ten have given a buy rating to the company’s stock. Skechers USA has a consensus rating of Buy and a consensus price target of $30.37.

Skechers USA Inc. (SKX) Downgraded by Morgan Stanley - Ticker Report

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

The Trends

As you can see from Diagram 1, during a long period of time, Skechers bounced up and down on expectations and uncertainties about future revenue and net profit growth. Finally, on July 22, 2016, the stock plunged below $25 per share because the company missed the expectations.

Despite that, I would like to look at the situation from a different angle and focus on the results themselves. In my opinion, there are five main reasons why Skechers' results look better than most investors think:

1. In Q2, the top line has increased by more than $77M year-over-year, or by ~10%. The six-month sales, as a result, have increased by more than 18%.

2. The Q2 net income has decreased by ~7% YoY, while the six-month net profit is still impressively 26% higher than a year before.

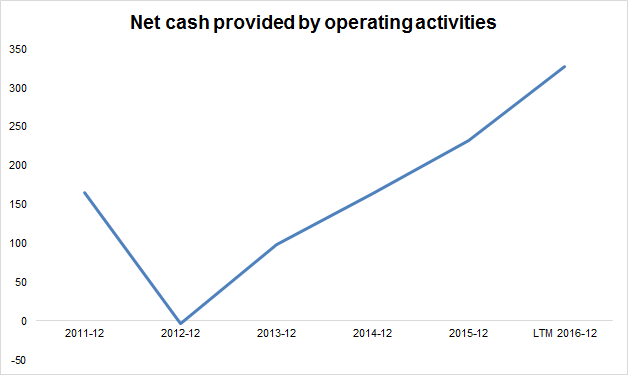

3. The cash flow from operating activities has been rising for more than four years! In this year, the figure has increased by more than 41%.

4. The margins are good. They have been increasing for almost six years. The net profit margin of 7.8% is surely lower than Nike's (NYSE:NKE) 11.6% or the industry's average of 8.9% but is still quite high and growing. Moreover, even with such margins the company shows great net profit growth, which is one of the highest in the industry (see Diagrams 3, 4).

5. The working capital management during this year has been efficient. The last-twelve-months' cash conversion cycle has decreased to 108 days from 116 days at the end of FY2015. Moreover, the main driver of this contraction is the decrease in inventory turnover by more than 16 days, or by 12%+.

Diagram 2.

Revising My Take On Skechers - Why The Buyer Gets It All - Skechers USA Inc. (NYSE:SKX) | Seeking Alpha

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

Q3 adjusted EPS was affected by one-off factors. The bottom line was affected by a higher tax rate that stood at 24.2% in Q3 2016 vs. 17.7% a year ago and 18.9% average for the last eight quarters. Also, there was the negative currency impact on International sales of $15.9mn. The U.K. shipped more than 1.2m pairs, a 20% increase y/y, but $ sales grew only 11% due to the weaker pound. Even if we strip off just the FX effect, EPS would have been $0.46, flat year-over-year and in line with the Street. The company's outlook is not that grim as it seems at the first glance. Management guided $710-735mn revenue in Q4 2016 with the midpoint of $722.5mn approximately 10% below the ex-ante consensus estimate, and implying no year-over-year revenue growth. A dip in year-over-year sales growth can be explained by the ongoing transition of several international distributors to a JV model. Revenues are recognized at the moment of shipment from factories for distributors and at the moment of the ultimate sale to consumers for JVs.

Given that Q4 is typically the strongest for distributors, while Q1 is stronger for international JVs and subsidiaries, this transition will result in that some part of Q4 2016 revenues probably will be transferred to Q1 2017. Israel was transitioned into a JV in Q3 2016, and SKX currently is in the final stages of South Korea moving to a JV as well. That implies that a weak Q4 revenue guidance is just a bump and international growth story is intact.

Why Skechers's Q3 Results Were Not So Bad - Skechers USA Inc. (NYSE:SKX) | Seeking Alpha

|