Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

By Alan Wheatley, Global Economics Correspondent

LONDON | Sun Mar 31, 2013 3:02pm EDT

(Reuters) - ‘Historic' is an overused word. But if the Bank of Japan meets expectations and embarks this week on a radical policy shift to crush deflation, the meeting will go down as, well, historic.

Because of gently falling prices, Japan has not grown in nominal terms for two decades, reducing its relevance for the global economy.

But all that could change if the BOJ's new governor, Haruhiko Kuroda, shows he is indeed serious about hitting the central bank's new inflation target of 2 percent.

"This is their best shot at reviving the economy," said Jerry Webman, chief economist at OppenheimerFunds in New York. "Even a modest improvement in the world's third-largest economy is going to add ... to overall global growth."

At a two-day rate review that ends on Thursday, the central bank is likely to start open-ended asset purchases immediately, rather than from 2014. The BOJ will also probably extend the maturity of the bonds it buys and set a new policy target focusing on the size of its balance sheet, sources familiar with the bank's thinking told Reuters in Tokyo.

Japan badly needs nominal gross domestic product to start expanding again so that the government's debt does not become unbearably large as a share of GDP. It is already dizzyingly high at 235 percent of annual output.

Rising prices also transmit signals about which sectors can most profitably deploy capital and labor. When deflation is entrenched, those market messages are muffled; stagnation sets in, as it has in Japan.

Despite the strong political mandate from Prime Minister Shinzo Abe, many doubt Kuroda will succeed in reflating the economy without more fundamental reforms such as injecting more competition into the economy and attracting more direct foreign investors - something Japan has shown little appetite for.

Even if his strategy does work, there could be a backlash from Japan's growing legions of pensioners, who have no interest in seeing their wealth and fixed incomes eroded by inflation.

All told, the stakes for Japan are arguably greater than at any point in the last fifty years, according to James Malcolm, a foreign-exchange strategist with Deutsche Bank in London.

He said those expecting to be disappointed by Kuroda's debut are themselves likely to be disappointed given the single-minded resolution to defeat inflation that Abe has shown since taking office in December.

"This is a product of the increasingly widely recognized failure of every other economic policy approach, presenting an opportunity that Abe has grabbed with both hands," Malcolm, a long-time Japan watcher, told clients.

DRAGHI IN THE SPOTLIGHT

While Kuroda has Federal Reserve Chairman Ben Bernanke's template for quantitative easing to follow, the BOJ chief's commitment to end deflation ‘at any cost' has echoes of European Central Bank President Mario Draghi's vow to ‘do whatever it takes' to preserve the euro.

The single currency has had another near-death experience over the terms of a rescue for Cyprus, and Draghi is sure to be quizzed about the deal's implications for the euro zone at a news conference following an ECB policy meeting on Thursday.

In exchange for a bailout loan, the International Monetary Fund, the European Commission and the ECB wiped out Cyprus's senior bond holders and imposed a levy on big depositors at the island's two largest banks. Temporary capital controls are also in place.

These unprecedented steps could yet prove contagious, touching off a deposit flight from weak banks in more important economies that could cause the euro zone to disintegrate, pessimists fear.

Optimists retort that the ECB has slung a safety net under the euro by promising to buy struggling governments' bonds as a last resort.

Where both camps agree is that Cyprus's crisis will deal a fresh blow to confidence and further delay the euro zone's recovery.

"Even without some sort of break-up or fragmentation, the economic outlook for the region is very poor given the fundamentals," said Jonathan Loynes with Capital Economics, a London research outfit.

EURO ZONE, U.S. JOBS DATA

The ECB is unlikely to deliver fresh monetary stimulus, according to economists, even though figures on Tuesday are expected to show that unemployment in the 17 countries sharing the euro rose to a record 12 percent in February. In Spain and Greece it has surged to around 25 percent.

Relief is unlikely any time soon, according to the International Confederation of Private Employment Agencies in Brussels, which represents 140,000 private firms around the world. Demand for agency jobs fluctuates roughly in time with changes in GDP and is a leading labor market indicator.

Denis Pennel, managing director of the group, said his members had lately been reporting weakness in Europe, with the biggest drop in demand in Italy and France. "We don't expect any recovery before the last quarter of this year at the earliest," he said.

Nor was business at job agencies in Japan looking up. "If you want to have signs of optimism, you should really look to the U.S.," Pennel said. The confederation's American members reported a 2.4 percent year-on-year rise in demand in March.

The Institute of Supply Management's manufacturing survey and non-farm payroll figures, both for March, are the conventional U.S. data highlights of the week. Employers are likely to have added 200,000 jobs, down from an unexpectedly large 236,000 increase in February, according to economists polled by Reuters.

Webman with OppenheimerFunds acknowledged that there had been some recent softness in the economic news flow but drew comfort from evidence, notably in the fourth-quarter GDP report, that U.S. firms are starting to invest some of their huge cash holdings.

"The economy is growing decently, but it's not really accelerating to any marked degree," he concluded.

(Editing by Patrick Graham)

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

This is is a guest post from Philip Pilkington, a writer and research assistant at Kingston University.

In January of this year I noted that the Japanese government was embarking on a stimulus programme and briefly enquired into whether it would likely work or not . At the time media commentary was mixed. Some were saying that it would be a complete failure while others were overflowing with optimism. I was slightly more reserved.

The problem with Japan is that they seemed unable to get consumers to open their wallets for any sustained period of time. In 2009 when the Japanese government ramped up spending in response to the 2008 downturn the economy picked up briefly. However, once the government retracted its spending the economy fell back into a slump as consumers retreated back into their characteristically frugal state.

In the above piece I noted that the best approach for the Japanese government would be to undertake a far larger direct fiscal stimulus program. However, since this was unlikely to happen I considered how far they might get with a limited stimulus combined with a devaluation of their currency that would promote Japanese exports. I pointed out that the yen had strengthened in relation to the dollar since the last stimulus in 2009 and that to even get back to those levels it would need to devalue by another 10 per cent. As of this week that devaluation has taken place and the yen is back to roughly 2009 levels versus the dollar – whether this will be enough to promote the export growth needed for recovery is another question entirely.

In the meantime, however, attention has turned away from the fiscal stimulus and towards the latest round of Quantitative Easing that has been announced by the Japanese central bank. The bank last week promised to double the monetary base over the next two years. In response to this news market speculation has, as previously mentioned, driven the yen back to 2009 levels against the dollar. It had been stuck above this for the past few weeks.

So far, so good; but the real question is: will the latest QE program have anything more than short-term effects on the strength of the yen? After all, the Bank of Japan started these QE programs back in 2001 and they have not met with much success. Sure, an announcement that they are doubling the monetary base may cause market speculators to sell the yen in the short-run, but can these effects be sustained or should we focus our attention on more fundamental issues?

The best measure of the extent of QE in Japan at any given moment in time is probably the most direct: that is, the level of “current account balances” of the commercial banks. As the Federal Reserve Bank of San Francisco notes, it was by increasing these current account balances that the Bank of Japan initiated their QE programs.

Since the fall in the yen is perhaps the most immediately obvious effect of the recent QE program let us first take a look at how this relationship has played out over the last decade and a half in Japan.

As previously noted the BoJ undertakes QE by increasing the “current account balances” – the red line. As we can see the program was run from March of 2001 until early 2006 when the bank quickly sucked cash out of the system by reducing the current account balances. QE then began once again rather slowly in 2008 and the sped up in late 2010.

Certainly it is true that the yen has weakened over the period of QE. However, on careful examination it should be clear that this weakening started in late 1999, at least 18 months before the first QE program. In addition to this when the Bank of Japan cut back on QE in early 2006 the yen continued to depreciate. The yen also sharply appreciated in the third quarter of 2008 despite the fact that this was when the Bank of Japan began another round of QE – this was, however, probably due to the markets racing to hold liquid assets as the 2008 financial crisis shook the world.

All of this considered it seems that while the yen has indeed been in a downward trend in the period of Japanese QE, it is by no means clear that the weakening was due to the QE. Indeed, careful examination of the above graph makes one rather sceptical that the QE program had significant long-term effects on the value of the yen at all. This should be kept in mind as the markets obsess over the short-term weakening of the currency that we have seen over the past few days.

Japanese officials are also hopeful that the latest round of QE will have substantial effects on inflation, which has been dipping in and out of negative rates in Japan over the past two decades. Again we can plot the inflation rate against the current account balances in order to see if the QE programs have had any substantial effects.

As was the case with the exchange rate, the effects that QE has had on inflation since it was initiated in March 2001 are extremely unclear. When the program was initiated the economy was experiencing deflation and it is not clear that this deflation was overcome at all between 2001 and 2006. Pointedly, however, less than 18 months after the BoJ halted the program in 2006 the economy experienced a short-lived spike in inflation. This seems to strongly suggest that the rate of inflation has no positive relationship to the current account balances at commercial banks. This should lead us to conclude that the QE programs do not have any appreciable effects on the rate of inflation.

Some may have also noticed that Japanese stock markets rallied on the BoJ’s announcement last week. This has largely been following trend as the Nikkei has been gradually climbing on the announcement of the stimulus in January. However, the announcement of a new round of QE has certainly led to a short-term market rally. So, let us turn to the relationship between the Nikkei and the previous rounds of QE to see if there is any relationship.

Here we can detect some relationship between the two variables. It is clear that when the first QE program was initiated in 2001 the stock market was in the dumps. As the current account balances at commercial banks piled up the stock market began to rise. It is also clear that it took some time for the stock market to respond to the first round of QE. The stock market only began to truly rise two years after the program had been initiated and only after it kicked into high-gear around the start of 2003. The stock market rising together with the rise in current account balances (i.e. QE) can be seen between the two black lines on the above graph.

If we consider that the latest round of QE was only really stepped up in late 2010 we might conclude that, given the two year lag of the last rally, the present stock market rally in Japan may actually be sustainable. This is not to say, of course, that people should dump all their savings into the Nikkei but the data does suggest that there is a relationship between QE and stock markets, although it is by no means clear how strong this relationship is. However, it seems that we can say with some confidence that QE can drive stock prices; certainly we can be more confident of this than it having any sustained effects on inflation or the exchange rate.

This is not particularly surprising. When the banks are flush with cash there is every reason to think that they will seek to move into riskier assets in order to try and earn a decent return; thus a rally in equities makes sense. This rally can then build momentum so that even when the QE is scaled back, as it was in early 2006, share prices can continue to climb until they are interrupted by something else – which, in the case under scrutiny, was the 2008 financial crash.

All in all it is unlikely that the BoJ’s latest QE program will have any substantial effects on the real economy. For such effects we need to focus firmly on the level of investment and consumption activity together with the trade balance. However, the QE program does seem likely to be able to support Japanese share prices to some extent; although we should naturally be cautious in making any firm predictions in this regard.

One more note on the Japanese trade balance. Although the current account has recently swung into surplus on the back of a weakened yen, the trade balance remains in deficit. This is because, since the Fukushima disaster in 2011, the Japanese have had to import far more fuel and gas. While it remains unclear when they will get their nuclear reactors back to full capacity their doing so should be considered a major signal that economic growth might return to the Eastern island. Such a consideration also provides a strong case for why the Japanese government should extend their stimulus program to promote green energy programs moving into the future. Yet another example, as if we needed one, that the problems faced by most developed economies today have far more to do with deficient demand and resource misallocation than they have to do with anything that takes place on the reserve accounts of commercial bank computers.

Posts: 2,904

Threads: 58

Joined: Mar 2012

Reputation:

259

I fear the stock market positive response to the quantitative easing is simply a reflection of more money being spent at the NIKKEI casino as opposed to more money being actually invested in economic growth (i.e. demand and subsequent supply). This I fear has been the case with the US economy. Wall Street is no longer about being a source of funds for growth capital. It is now largely a playground for the "investing" public and more money into the economy just provides stock market price inflation.

When you think about it, how many companies have you seen in a negative light when the need for a secondary is mentioned? Say the word "secondary" and investors scatter these days. Announcing a secondary is like declaring yourself a leper. Shouldn't raising capital through secondaries be seen as a primary purpose of the stock exchanges and thus a good thing?

What's my point? I don' know. IOC's secondary was put to good use finding more gas. Japan needs that gas to grow their economy. How does Japan finance that purchase? Doesn't really matter to me I guess so long as IOC is the supplier.

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

04-11-2013, 02:48 AM

(This post was last modified: 04-11-2013, 02:49 AM by admin.)

'ArtM72' pid='20471' datel Wrote:I fear the stock market positive response to the quantitative easing is simply a reflection of more money being spent at the NIKKEI casino as opposed to more money being actually invested in economic growth (i.e. demand and subsequent supply). This I fear has been the case with the US economy. Wall Street is no longer about being a source of funds for growth capital. It is now largely a playground for the "investing" public and more money into the economy just provides stock market price inflation. When you think about it, how many companies have you seen in a negative light when the need for a secondary is mentioned? Say the word "secondary" and investors scatter these days. Announcing a secondary is like declaring yourself a leper. Shouldn't raising capital through secondaries be seen as a primary purpose of the stock exchanges and thus a good thing? What's my point? I don' know. IOC's secondary was put to good use finding more gas. Japan needs that gas to grow their economy. How does Japan finance that purchase? Doesn't really matter to me I guess so long as IOC is the supplier.

Yes, Art, those secondaries. Companies still do them, and there has been a bumper issuance of corporate debt due to the low interest rates, but probably the casino elements of stockmarkets have taken over.

What happens in Japan is the most interesting, and important economic experiment of our time:

-

Two 'lost' decades (they're not that lost, on closer inspection) have shown that balance sheet recessions after financial bubble burst (the Japanese crash in the early 1990s was three times the relative size of the US crash in 2008/9) has a habit of not curing itself easily, especially when deflation and deflationary expectations is ingrained and interest rates are at the zero bound

-

Probably only really outsized measures can break the vicious cycle, Japan. Krugman urged them to do what they're going to do now as far back as 1997, and waiting that long the risks of drastic reflation have considerably increased, as the size of the outstanding public debt has balooned. Drastic reflation bears the risk of a bond market rout (people like Kyle Bass are betting on one, although he has done so for quite some time already)

-

The US is in far better shape, as much more decisive actions were taken in the immediate aftermath of the crisis, but a considerable amount of the balance sheet recession dynamic lingers on, so we have much to learn from what is going to happen next in Japan. It's a sort of open air lab for us.

-

I would say, on evidence (some of that above), doubling the monetary base in two years might not work outside of the realm of the Nikkei. For some time, I have been of the opinion that it's probably necessary to monetize part of the public debt directly

For the uninitiated, what is a balance sheet recession?

This is the situation in which the private sector saves so much more than it invests (in an effort to repair balance sheets which were greatly damaged by a financial crash) that interest rates have to be deeply negative in order to equate the two. Since the latter isn't possible, there is a bit of a policy problem. Doing nothing isn't an option because the private sector savings glut will drive demand downwards (a process that can feed on itself), somwhere, the shortage of demand has to be compensated.

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

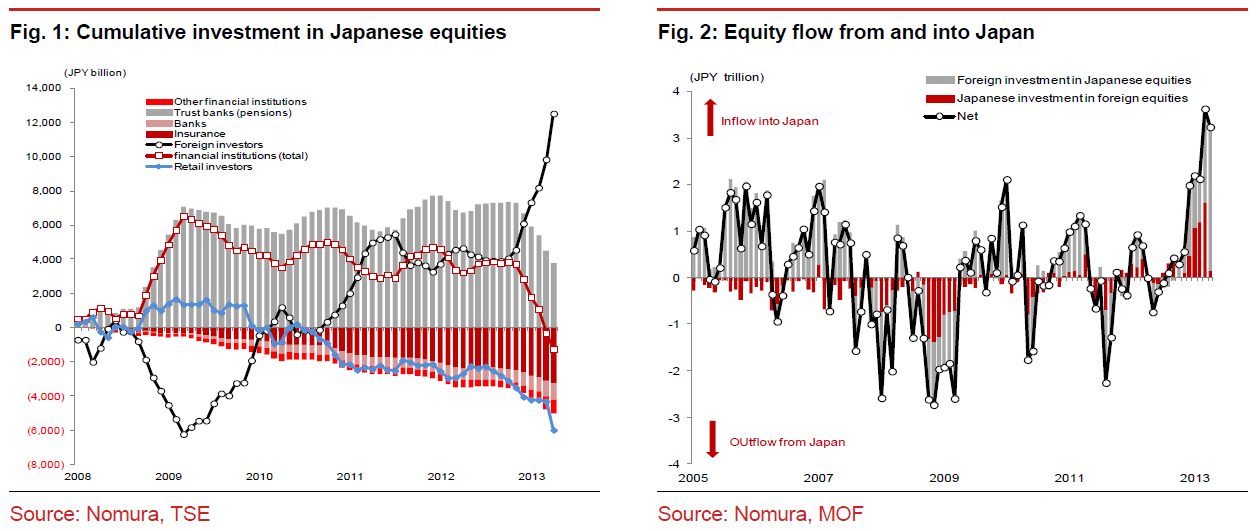

Spot the outliers:

That chart, from Nomura, shows the main driver behind the super soaraway Nikkei which is up 45 per cent since the start of the year — foreign investors. They have been buying up Japanese equities since last October to the tune of Y8.6tn. Domestic investors, mostly pension funds, have stood at the other side of the trade, selling Japanese and foreign equities.

And that should be supportive for the yen, right? We’ve had a total inflow into Japan of more than Y3tn in March and April putting the Japanese trade deficit of Y1tn per month into context.

But, say Nomura, the impact on the yen isn’t clean and is probably counterintuitive (our emphasis):

[W]e need to consider the impact of FX hedging to get a true sense of the net FX impact of the various equity-related flows: First, currency hedging by foreign investors when investing in Japanese equities will reduce the impact of fresh inflows on the yen. Second, hedge rebalancing in line with rising equity prices will also lead to JPY selling (simply to keep the hedge ratio constant for existing equity portfolio) [...]

We assume a 20% hedge ratio for foreign exposure in Japanese equities and 10% for Japanese exposure of foreign equities. These figures are based on company commentary as well as ad hoc surveys of selected real money clients. Meanwhile, we assume new flow into the Japanese equity market to be 50% hedged (a number broadly consistent with the distribution of flows into hedged and unhedged Japan equity ETFs: 57%). We assumed a lower hedge ratio for Japanese exposures as pension funds and retail investors (who do not hedge) have a larger share of foreign equities in Japan than elsewhere. To keep the hedge ratio at a constant level (20%), foreign investors have to sell JPY when Japanese equity prices rise (bigger exposure needs bigger hedging) and Japanese investors need to do the opposite. To simplify, we assumed the hedging adjustment happens every week although in reality the adjustment happens less frequently.

That all means that foreign equity investors have most probably been net sellers of yen, not buyers — yen selling to keep the hedge ratio at constant has exceeded yen buying from new investment in most periods, say Nomura.

Assumptions obviously matter, but unless you punt the hedge ratio down towards 10 per cent you still get net selling:

On the other side again are the Japanese equity investors, who have been buying yen as they have been selling foreign equities and higher equity prices globally are assumed to require more FX hedging, which means yen buying.

Nonetheless, Nomura estimate their pace of yen buying to be slowing as rebalancing by pension funds is slowing and equity performance outside Japan is less impressive than Japanese equity performance.

So we probably have dominant yen selling overall and that could grow if Japanese equities stay bought and/ or foreign investors boost their hedge ratios.

Nomura (who are Japanese equity bulls) estimate that a 5 per cent increase in the hedge ratio would amount to Y6tn of yen selling while if Japanse equity prices keep rising Y2tn additional net yen selling is possible to just keep the hedge ratio constant if Japanese stocks rally another 5 – 6 per cent. Not impossible.

Opposite assumptions naturally apply and the relative performance of Japanese equities and global equities will also have an impact but it seems likely that right now, higher Nikkei means a weaker yen. God only knows what Akira Amari thinks about that.

Related links:

Assessing Abenomics – FT Alphaville

JGBs: “Yes I would, Kent” – FT Alphaville

Bird, plane, Abe – FT Alphaville

Kyle Bass bets on full-blown Japan crisis – FT

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

05-27-2013, 07:22 AM

(This post was last modified: 05-27-2013, 07:27 AM by admin.)

Shinzo Abe, the Japanese prime minister. (Photo: AFP)

Kudos to Kyle Bass at Hayman Advisers for warning that the Bank of Japan would lose control of its ¥70 trillion bond buying blitz. The spike in the 10-year yield to 1pc on Thursday was certainly shocking to behold.

His point is that the BoJ faces a “rational investor paradox”. The authorities are trying to drive up the inflation to 2pc and therefore to devalue Japanese government bonds (JGBs), so why on earth would you want to own them?

“If JGB investors begin to believe that Abenomics will be successful, they will ‘rationally’ sell JGBs to buy foreign bonds or equities,” he told Bloomberg

He says the scramble to sell has “overwhelmed” buying by the BoJ. Governor Kuroda will now have double down with a huge increase in the scale of QE.

The argument is similar to warnings by Nomura’s Richard Koo, Japan’s most famous economist and an arch-Keynesian. The two men reach the same conclusion coming from diametrically opposed theoretical starting points.

As I reported last night, Mr Koo thinks the Abenomics plan of monetary reflation is madness. “Once inflation concerns start to emerge the BoJ will be unable to restrain a rise in yields no matter how many bonds it buys.” This could lead a “loss of faith in the Japanese government” and the “beginning of the end” for Japan’s economy.

Mr Koo said the BoJ faces a “time inconsistency problem”, a variant of Mr Bass’s paradox. Markets react more quickly to events than the economy. “The Japanese authorities are trying to generate inflation first and then hope for recovery, which means debt service costs will increase before tax revenues do.”

This will worsen the debt trajectory, set to reach 245pc of GDP this year (IMF), roughly where Britain ended the Napoleonic Wars. But then Britain produced half the world’s manufactured goods in the early 19th century, so it may be tougher for Japan.

Mr Koo says “long-term rates may rise before the real economy”. If so lenders will respond to these signals more quickly that borrowers, choking credit.

He says Kuroda has “altered the market structure of the last two decades” and undermined a fragile equilibrium, inviting a speculative attack on the JGB market by foreign hedge funds.

So that then is the critique. I don’t agree that it is game over for Abenomics. My view is that the Keynesian doctrines of endless fiscal stimulus without monetary support advocated by Mr Koo over the years is the cause of Japan’s desperate crisis (though he says the economy could have achieved escape velocity long ago if they had done more of it, which is not as absurd as it sounds).

Au contraire. Monetary policy should take the strain, pursuing a nominal GDP target of 3pc and later 4pc to turn the vicious circle of the “denominator effect” (ie a rising debt load on a shrinking nominal base) into a virtuous circle.

This is what Takahashi Korekiyo achieved with such brilliance in the early 1930s, setting off a boom and falling debt ratios. Though he also forced the BoJ to finance fiscal spending too to kickstart recovery. I am not against that either if it works. In fact in it is a rather good idea (for Japan, not the UK obviously).

Mr Koo’s argument that balance sheet recessions require radical action by governments is correct, but I refute his claims that QE was tried and failed in Japan. It was never tried.

The BoJ meddled on the margins with pinprick purchases of short-term debt, buying from the banking system, and merely pushing up the monetary base. Of course it failed. Who cares about the monetary base. It is irrelevant.

What they should have done is to conduct old-fashioned open-market operations, à la Friedman, Fisher, Hawtrey, Cassel, or Keynes himself, buying long bonds from non-banks to force up the M3 money supply. That works, as Ben Bernanke discovered when he finally alighted upon the policy by accident late in the Fed’s QE efforts.

True, the ructions in Japan over the last few days have been extraordinary. Governor Kuroda was forced to reassure the nation on Friday that the BoJ has the instruments to restore order to the bond markets

Premier Shinzo Abe was very blunt in parliament, warning that “sharp increases in long-term interest rates could have a grave impact on the economy and the government’s fiscal conditions. We expect the BOJ to respond appropriately,” he said.

Mr Abe is not pleased, I would surmise, and quite understandably so since the BoJ seems to have cocked up badly. My guess is that JGB market will settle down once they work out how to execute the task.

I stick with my view that the BoJ has the means to crush all resistance, and should do so. This may require financial repression. Rutaro Kono and Makoto Watanabe from BNP Paribas have an excellent note out this morning arguing that Kuroda will have to copy the “pegging operations” of the Fed in the 1940s.

In effect, the Fed became part of the Treasury’s debt management team as the budget defict hit 25pc of GDP in WW2. It capped one-year notes at 0.875pc and 30-year bonds at 2.5pc. The markets knew that all necessary means would be used to hold the line (as the Swiss did in 2011 to hold the franc at 1.20 to the euro).

It certainly worked. It allowed the US to whittle away its wartime debt through inflation and negative real rates. The creditors paid the price. It was an “inflation tax”, or covert debt restructuring.

That is what lies in store for Japan, and it will be horrible for pensioners, savers, and those expecting an annuity. Whether the authorities can pull it off it without capital controls is an interesting question. My guess is that controls will be part of the mix in the end, and much else besides. Tough. Leaders don’t run countries for the benefit of markets.

But all this is clearly “doable”, and if the alternative is a spiral into mayhem and debt default, you can hardly blame Mr Abe for wanting to try. There was always a “Hail Mary” element to this massive reflation experiment, a last-ditch effort to avert a debt compound spiral.

The critics are right to say it may fail. But are they suggesting that the previous status quo was tenable? If Mr Bass happens to read this blog, I would like to know what he would do if he were prime minister of Japan.

As for the countless readers demanding an apology from me for backing QE, Abenomics, and all the sins of monetarism: I defy you all.

Read more by Ambrose Evans-Pritchard on Telegraph Blogs

Follow Telegraph Blogs on Twitter

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

This is the most interesting economic issue by far at the moment. We have Keynesians (Koo), a monetarist (Evans-Pritchard) and the Austrians (John Mauldin, Kyle Bass) weighing in. Jury still out, but on first evidence, we have to give it to Pritchard. Mauldin's piece can be read here, but it isn't quite clear to me what exactly he's proposing:

http://www.businessinsider.com/japan-eco...ter-2013-5

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

05-27-2013, 07:32 AM

(This post was last modified: 05-27-2013, 07:35 AM by admin.)

The most important issues are:

1) Can the BoJ control the JGB (the Japanese Government Bond) market?

Bass and Koo don't seem to think so but Pritchard comes with good examples to show that this is indeed possible.

2) Once unleashed, can the BoJ control inflation from spiralling out of control and keep it at 2-4%, a nice pace at which real debt burdens will dissolve slowly like snow melts in a pleasant spring sun?

That's a trickier question..

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

A thought is bubbling up. Supposedly, Kyle Bass' hedgefund (and we assume a host of others) are shorting JGB's, egged on by the likes of ZeroHedge. While we don't begrudge (almost) anyone to make a profit, this is one of these cases where success for the hedgefunds could possibly contribute significantly to economic distress in Japan, and by extention the world. If they contribute to a crash in the JGB markets, public finances in Japan become untenable, capital of Japanese banks disappears, pension funds will go bust, and this is the third biggest economy in the world we're talking about.

We've seen in the mid 1990s what havoc an implosion of a rather small economy (Thailand) could cause in terms of ripple effects, we've seen what Greece could do, an implosion of Japan is a disaster of unmitigated proportions, especially coming after such a fragile state of the world financial system and the world economy in general.

We're well aware that there are some who abhor what Abe and the BoJ are trying to do. What we haven't heard from those people (or from anyone else, for that matter) is what alternative they have. Don't hold your breath, that's basically because there isn't one.

Adam Smith set out a great case for free markets, they usually create benefits for all concerned (called the static and dynamic gains from trade). We've already argued that much financial activities create little in terms of gains from trade but are essentially zero-sum activities (my loss is your win, and vice versa), and some can be even considered negative-sum games.

We have a feeling that taking on (probably highly leveraged) bets against JGB's falls distinctly into the latter category. What if he succeeds, what does he accomplish (apart from making a really big profit)? Consider this:

According to the BoJ, a 100 basis-point increase in interest rates would lead to mark-to-market losses equivalent to 20 per cent of tier-one capital for regional banks – and 10 per cent for the major banks. [ FT]

if JGB interest rates rise 2% in Japan, then the government must pay almost 80% of its revenues (as currently received) just to cover the interest on its debt.

We'll spare you what happens to their pension funds (simply because we don't have data on that), but it can't be pretty. Financial markets do have useful functions, we're the last to deny that. They allocate capital, they price risk, they provide liquidity and funds where needed, but in this case, we're hard pressed to see any benefit of shorting JGB's.

If Kyle Bass succeeds, he'll significantly contribute to wrecking the third biggest economy in the world. Do we really want him to succeed? The outcome of that is that a few men will get astronomical amounts of money, while Japan will be plunged into misery and it's very plausible that the whole world economy will suffer.

Is that a rational outcome? Is that how capitalism is supposed to work?

Standing in his way is the BoJ, the Bank of Japan, the one big buyer of JGB's at the moment. We better hope it succeeds..

Posts: 12,025

Threads: 1,809

Joined: Apr 2008

Reputation:

227

One could argue that in the case of the eurozone, shorters of peripheral bonds were still providing a "service," as they forced governments (and, more importantly, the ECB) to act and there were still avenues for action.

But in the case of Japan, there is nothing they can do that they're already doing. Yes, structural reforms will be good, but they have a pay-off that's slow, gradual, and years off, this won't help if Japanese public finances derail.

Even Kyle Bass good friend, John Mauldin, argues that they are backed into the mother of all corners..

|