How to escape from the slow-growth doldrums

More than six years after the Great Recession's end, economic growth in the U.S. remains lackluster. That's raising concerns among economists that the U.S. is entering a period known as "secular stagnation," an idea first proposed by Alvin Hansen in 1938 and recently revived by Larry Summers.

When an economy enters such a period, it's caught in an extended period of low economic growth. Summers believes the U.S. and other economies may be suffering from this ailment, though it's too soon to know for sure.

To understand the nature and cause of secular stagnation -- and solutions to it -- a simple example might help.

Imagine an economy with no imports and exports, perhaps an isolated island with no way of trading with other islands that produces $100,000 in goods and services each month. One of the most basic concepts in macroeconomics is that the total value of income equals the total value of production, so in this economy the total income of the residents would also be $100,000.

That's because when a good is produced and sold, the income the firm receives is paid out in wages, interest and rent, and whatever is left over is profit (which could be negative). Thus, the value of the good that is sold turns into income of some type.

When goods are held in inventory, things get a bit more complicated, though the result is the same. So, we'll assume no inventories to keep things simple.

Now suppose the island's residents spend $90,000 of their income on goods and services, and save $10,000. Wouldn't that create a problem? There's $100,000 worth of goods and services available in the economy, but only $90,000 in spending. How do the rest of the goods get purchased?

The answer is that $10,000 in saving gets turned into investments through financial markets. This is one of the main functions of financial markets: to find a way to turn saving into productive investments.

Let's assume in this economy, there's $5,000 in deprecation each month, so $5,000 of the $10,000 in saving is used to replace worn out capital, and the other $5,000 is used to purchase new capital that can be used to produce even more in goods and services. Again, to make it simple, assume that the $5,000 in new capital will increase output in the next period by $5,000.

Thus, in the next month, GDP for this economy would increase to $105,000 (a 5 percent growth rate), and the process would repeat. Part of the $105,000 in income will be used for consumption, and the rest will be saved. Financial markets will turn the saving into investment, which covers depreciation from the last period and new investment in the current period. The new investment allows the economy to produce even more, and so on, and so on.

But what if something goes wrong? What if financial markets fail to turn all of the saving into investment?

Let's start with the first month once again, which has $100,000 in income, $90,000 in spending and $10,000 in saving. Suppose something goes wrong so that only $5,000 is turned into investment -- just enough to cover depreciation, but not enough for any new investment -- and the other $5,000 sits idly in banks as excess reserves.

In this case, with no new capital, there would be no growth. So, in the next period, production and income would be $100,000 once again.

The failure of financial markets to turn all of the saving into investment results in zero percent growth instead of the 5 percent growth realized when all of the saving was utilized.

If less than $5,000 of the $10,000 is turned into investment, the economy can't even cover depreciation, and growth would be negative. If more than $5,000 is utilized, but less than $10,000, there would be some growth, but it would be less than 5 percent.

If this continues period after period, it becomes an instance of secular stagnation.

Classical economists did not believe this could happen. They argued that financial markets would always find a way to equate saving and investment.

The key is movement in the interest rate. Interest is the reward for saving. When interest rates rise, people tend to save more. However, interest is also the cost of borrowing the funds needed to make an investment, and when interest rates go up investment tends to fall (borrowing costs are higher, so fewer projects are expected to be profitable).

Saving and investment are equated through market forces that move the interest rate up and down. For example, if saving is less than investment, interest rates will tend to increase, causing saving to rise and investment to fall until both are equal. In the opposite case, interest rates will decrease until saving and investment are aligned.

The essence of this argument is no different than the usual supply-and-demand models. If supply is greater than demand, prices fall; if supply is less than demand, prices rise and bring the market back into equilibrium. Just think of the interest rate as the price of money.

There is no practical limit to how much interest rates can increase, but they can fall only so far. The "zero lower bound" (ZLB) constrains how low interest rates can go (if they're negative, you can borrow money, then pay back less than you borrowed -- but why would a lender want to do this?). I'm omitting some technical points: The bound isn't exactly zero, and the Fed has ways to produce negative interest rates, but it hasn't been willing to do that, so the ZLB has been an effective constraint.

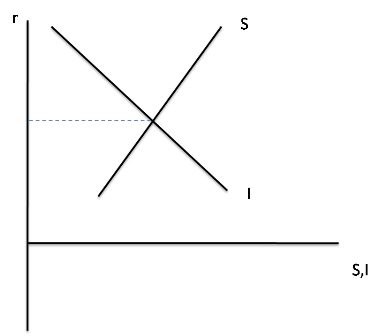

The following two diagrams illustrate the secular stagnation problem. Both show how saving (S) and investment (I) change with the interest rate ®, as just described, and the intersection of the two lines is the equilibrium point. The first diagram shows normal times:

In this case, the classical argument is correct: Market forces will push the interest rate to the point where saving and investment are the same (think of this as the $10,000 in saving being turned into investment in the first example above).

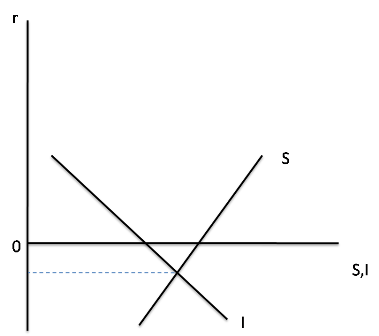

But in a recession, the investment curve shifts inward as businesses foresee poor economic conditions ahead and invest less at every interest rate. In a big recession, like the one we just had, it's possible for the investment curve to shift inward by a large amount, so large that the equilibrium interest rate is negative:

In this case, the interest cannot fall enough to equate saving and investment because it's limited by the ZLB. When the interest rate falls to zero and gets stuck there, saving will be greater than investment (on our island, this is the case where saving is $10,000, but investment is less than that). So long as the economy is stuck in this trap, it will experience stagnant growth. Investment and growth would be higher if the economy could somehow reach the equilibrium point.

What's the solution to this problem? There are two ways the equilibrium could be returned to a positive interest rate. The first is to shift the saving function inward. If policy could cause this to happen -- a tax on saving perhaps -- it would work, but in this case investment would fall even further. A better solution would be to shift the investment function outward.

How can this be accomplished? Investment is the sum of private sector investment plus public sector (government) investment. Private investment could be increased by lowering the interest rate with monetary policy, but since the interest rate is as low as it can go, this won't be effective.

Another solution is to raise private investment through mechanisms such as tax incentives. But in a stagnating economy, business confidence is low, and it's unlikely this will have much of an effect. It's worth trying, but it's unlikely to be enough.

Yet another solution is to raise public investment; infrastructure spending is a frequently mentioned candidate. This is attractive for two reasons. First,investment in U.S. infrastructure has been lagging, which needs to be addressed independent of the secular stagnation problem. Second, while tax incentives amount to leading a horse to water and hoping it will drink, government investment is determined by fiscal policy. It can be whatever value Congress and the president want it to be.

This is why those who are worried about secular stagnation have repeatedly called for substantial investment in infrastructure.

To repeat, we do not yet know if the U.S. in a secular stagnation episode. But if it is, the time to act is now. The longer we wait, the harder it will be to overcome. Since the country needs infrastructure spending in any case, why not use it as insurance against this possibility?