Always interesting…

NGL to the Rescue, Revisited (Part 1/2)

Posted by Rune Likvern on January 28, 2011 – 10:59am

DISCLAIMER: The author holds no positions in the oil/energy market that may be affected by the content of this post.

This is the first of two posts where I present a closer look at NGLs. In this first post I will present a closer look at volumetric energy (heat) content for some hydrocarbons in liquid state and the wetness factor for natural gas. Later I will present a closer look at the conditions that need to be met to make the IEA’s NGL projections happen. In the posts I have adhered to the IEA’s definition of NGLs as far as the actual data has allowed.

The International Energy Agency (IEA) projects in its World Energy Outlook for 2010 (WEO 2010) New Policies scenario (NP) that the Natural Gas Liquids (NGLs) portion of total world volumetric liquid energy supplies will grow from 13% in 2009 to 19% in 2035.

The WEO 2010 forecasts that more than 50% of the growth in world volumetric liquid energy supplies will come from NGLs. More than 90% of the growth in NGLs is forecast to come from OPEC.

- NGLs have around 60 – 70% of the volumetric energy (heat) content of crude oil.

The above fact seems to get lost in debates about liquid energy supplies.

- The wetness factor of natural gas needs to develop according to expectations derived from the IEA WEO 2010.

- Growth in world production of natural gas needs to closely match the forecast.

IEA WEO 2010 definition of natural gas liquids:

Natural gas liquids (NGLs) are the liquid or liquefied hydrocarbons produced in the manufacture, purification, and stabilization of natural gas. These are the portions of natural gas which are recovered as liquids in separators, field facilities, or gas processing plants. NGLs include but are not limited to ethane, propane, butane, pentane, natural gasoline, and condensates.

About two years ago I posted IEA WEO 2008 – NGLs to the Rescue which challenged the IEA’s forecast on future NGL production.

Relative to the IEA WEOs from some years back, the IEA has revised down future demand for liquid energy. The diagram above also shows the forecast from the Reference Scenario (RF) in the IEA WEO 2008.

The forecast from the IEA also acknowledges a future decline in non-OPEC crude oil supplies and globally a flat supply of crude oil towards 2035 and a strong growth in unconventional oil supplies.

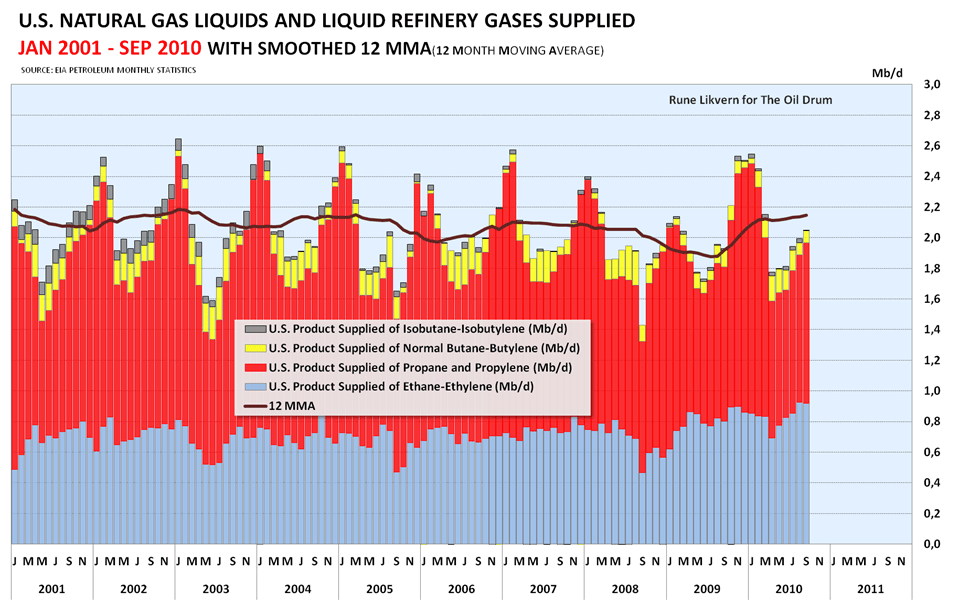

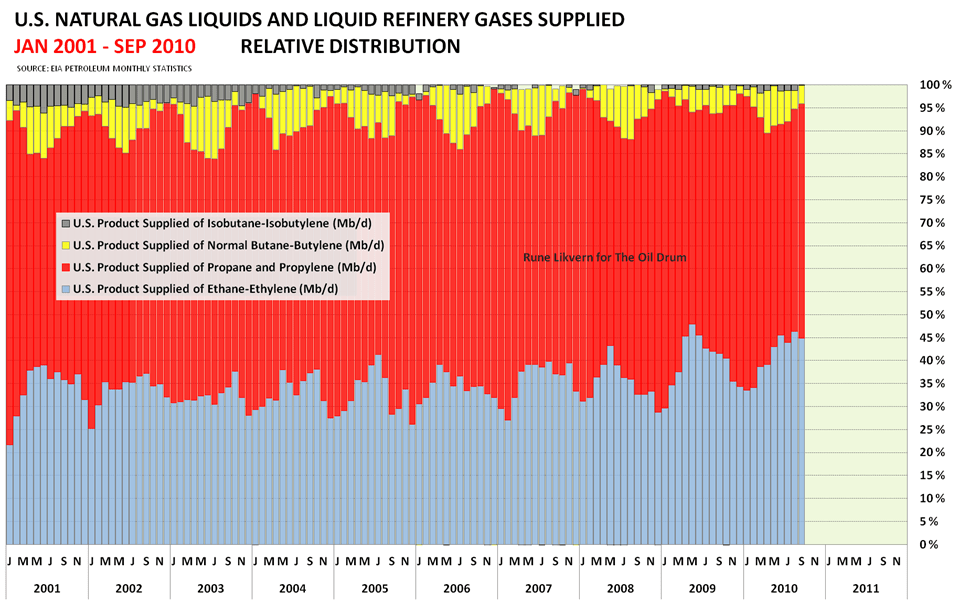

The graph above shows the world’s supplies of liquid energy as reported by the EIA. Figure 6 shows how these supplies would appear as NGLs and other liquid energy supplies converted to crude oil equivalents, i.e. heating value adjusted.

The graph also illustrates that with time the supplies of butanes have declined while there has been a growth in ethane. Ethane is primarily used as petrochemical feedstock, i.e. non-energy use.

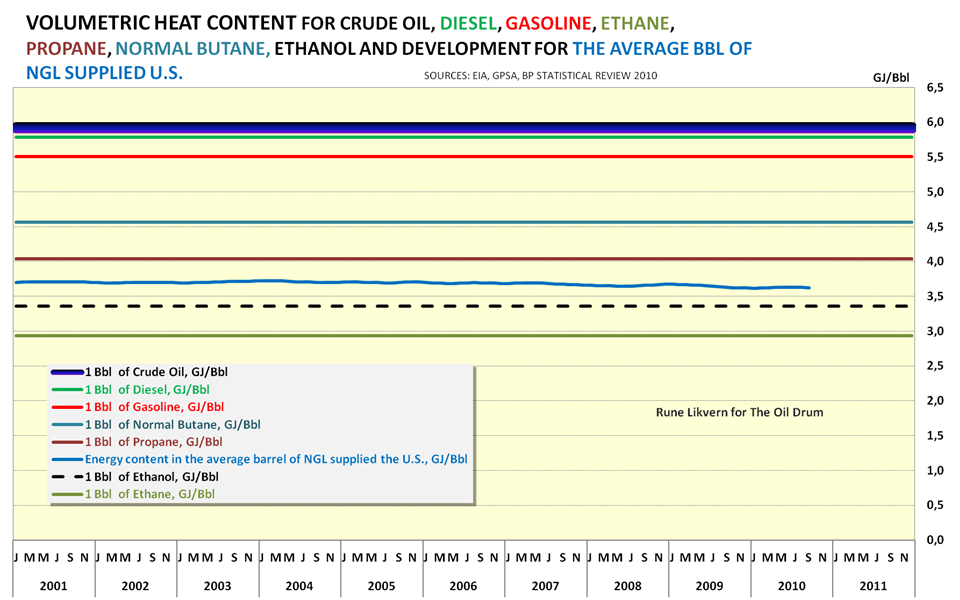

What can be perceived from the above diagram is that the “average bbl” of NGLs in the U.S. shows a declining heating value through time.

NOTE: Crude oils have a wider spread than depicted in the above diagram and the shown span in volumetric heating value is chosen for reasons of clarity.

The diagram also illustrates that as the number of carbon and hydrogen atoms declines, so does the volumetric heat content.

Refinery gains are mostly a form of double counting energy. The refining of crude oil involves breaking the long HC chains down to shorter chains and in this process, the resulting products have less volumetric heating content than crude oil and yield a higher volume.

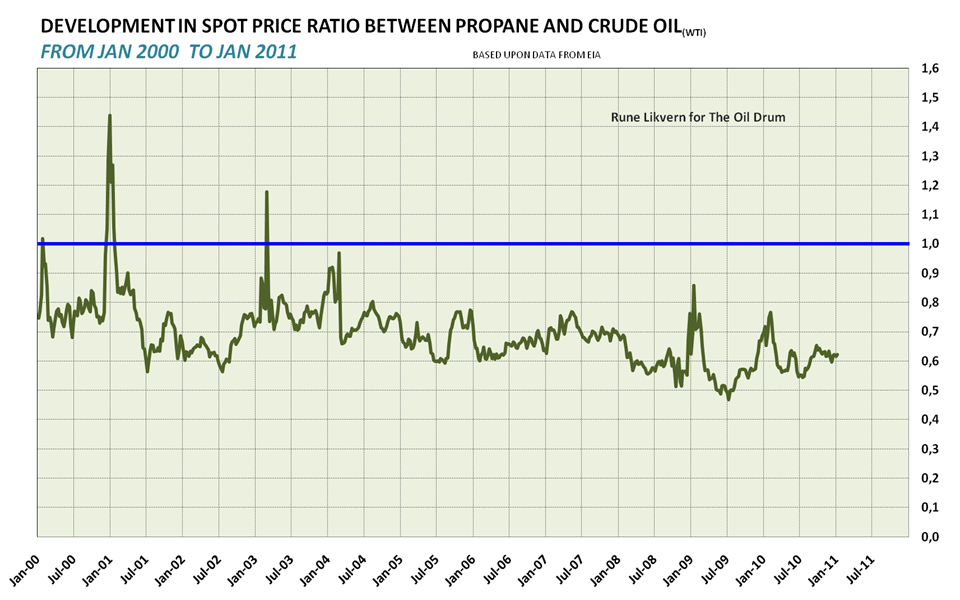

Some of the NGLs fetch a price relative to crude oil that reflects their volumetric energy content. This is illustrated below for propane.

One parameter that normally describes the development of gas fields is the wetness factor. Natural gas is a mixture of several light hydrocarbons, and specifications from customers and pipeline operators require that these are maintained beneath a specified limit to avoid the formation of liquid droplets during normal operating conditions. The heavier hydrocarbons that are extracted from the gas stream are commonly referred to as NGLs.

The wetness factor describes the relationship between sales gas and NGLs and how it develops over time. The more NGLs that a fixed volume of produced gas yields at standard conditions, the wetter it is considered. With time, the produced gas will normally become increasingly drier.

The owners of gas fields will normally search to develop the wetter fields first as these fields generate additional income from the NGLs. This is what is presently driving some of the shale developments in the U.S. as the operators go after what they refer to as the “sweet spots”.

As NGLs and condensates are not part of the OPEC quota system, this also gives OPEC members an incentive to extract these liquids to generate additional income.

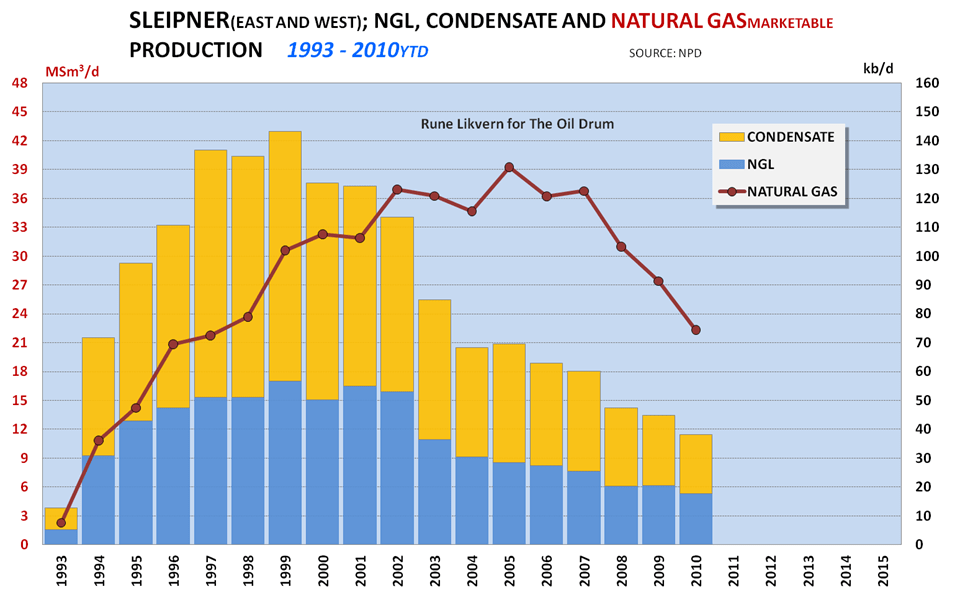

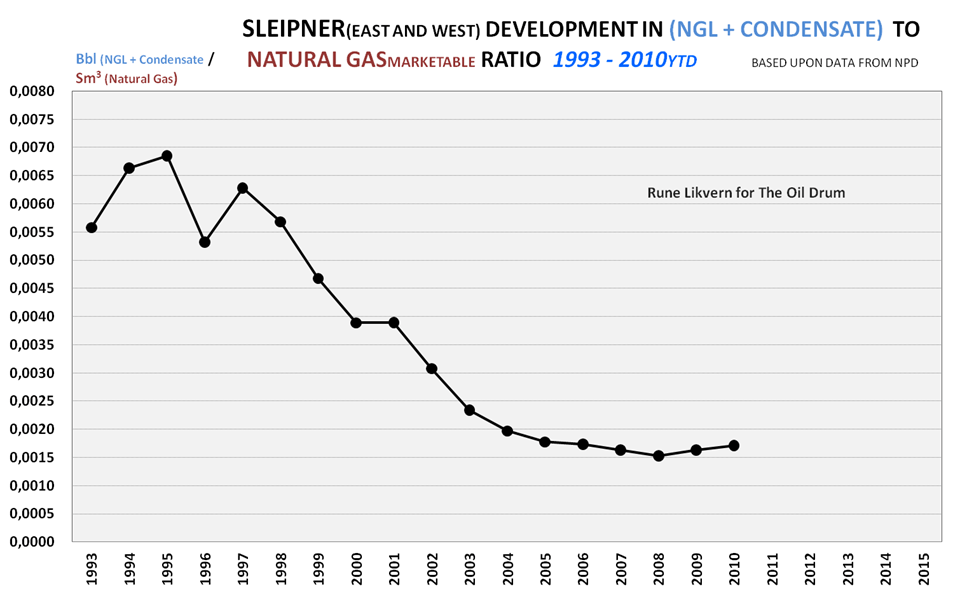

Development of the wetness factor for the Sleipner area serves as an illustration on how the wetness factor normally develops for a field.

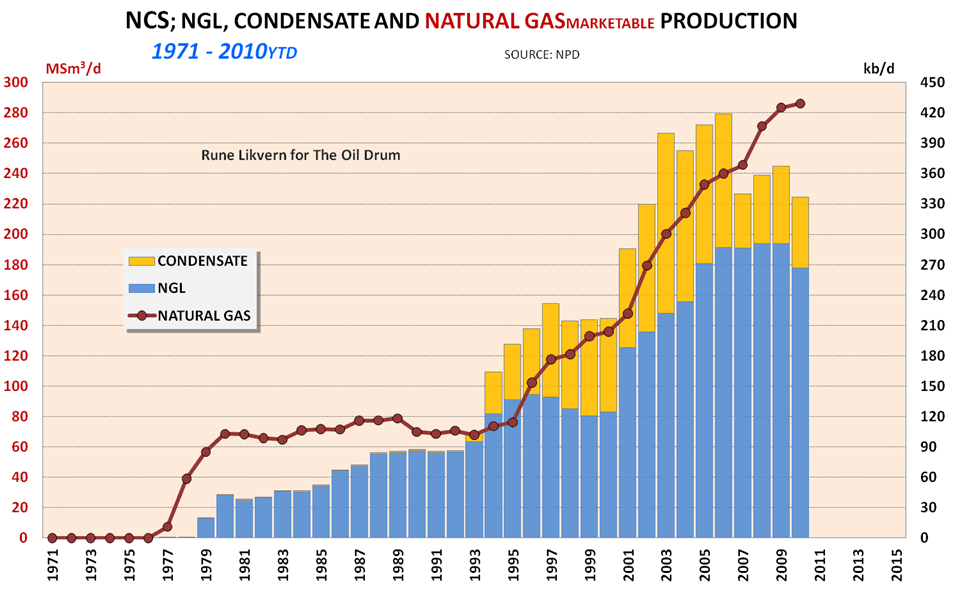

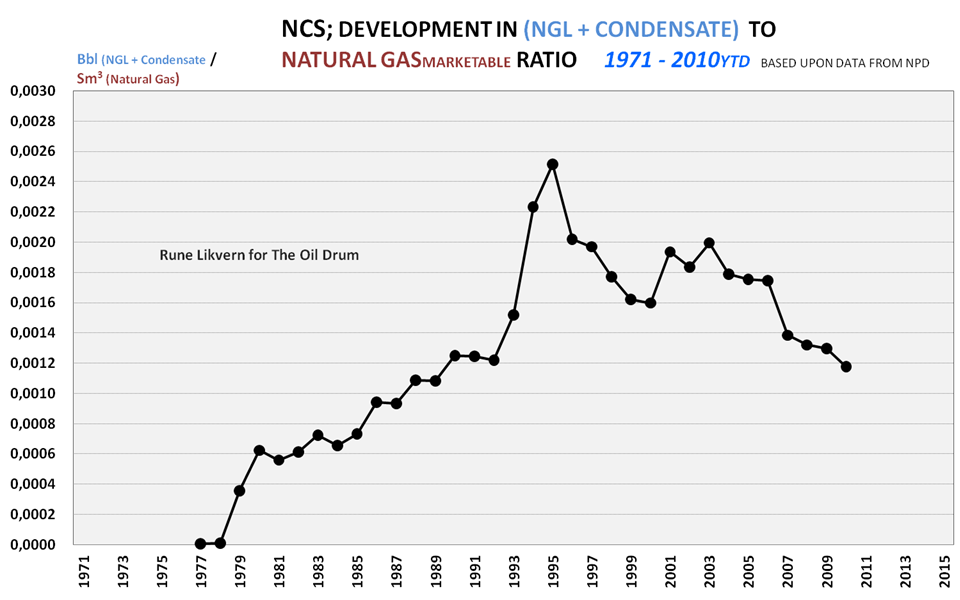

The chart above illustrates that the wetness factor for a region ascends towards a peak and then declines. It is now expected that the wetness factor for the NCS will generally continue to decline in the years ahead.

The diagram illustrates that the IEA expects the wetness factor for the world to grow in the years ahead. This is led by growth from OPEC while recognizing that the wetness factor will decline for non-OPEC countries in the years ahead.

Looking at recent developments, the wetness factor for Saudi Arabia has declined. The developments for Iran (South Pars) and Qatar (North Field) where the wetness factor has recently declined should be of particular interest.

Iran and Qatar held around 60% of OPEC’s proven natural gas reserves as of the end of 2009. These two countries are projected by the IEA to grow their natural gas production more than 100% towards 2035 and produce around 40% of OPEC’s natural gas.

Russia has what is considered a dry gas, reflected by the wetness factor.

As shown in this post, the wetness factor may wobble around and generally decline with time. It is still a little early to draw any firm conclusions about the wetness factor’s future development. However, if the wetness factor shows a general future decline this will impact the future supplies of NGLs.

In the second post about NGLs, I will present a closer look at natural gas production and reserves, and present the IEA’s forecast on natural gas production from OPEC, as these countries are forecast to have the strongest growth in future world NGL supplies.

SOURCES:

[1] BP STATISTICAL REVIEW OF WORLD ENERGY 2010

[2] IEA WEO 2006, 2007, 2008, 2009 and 2010

[3] EIA, INTERNATIONAL ENERGY STATISTICS

[4] EIA, INTERNATIONAL PETROLEUM MONTHLY

[5] GPSA, Engineering Data Book, SI units

[6] NPD, ACTUAL PRODUCTION DATA FOR NCS