Yes, the banks are in bad shape, but not that bad…

First, the article, followed by our comments.

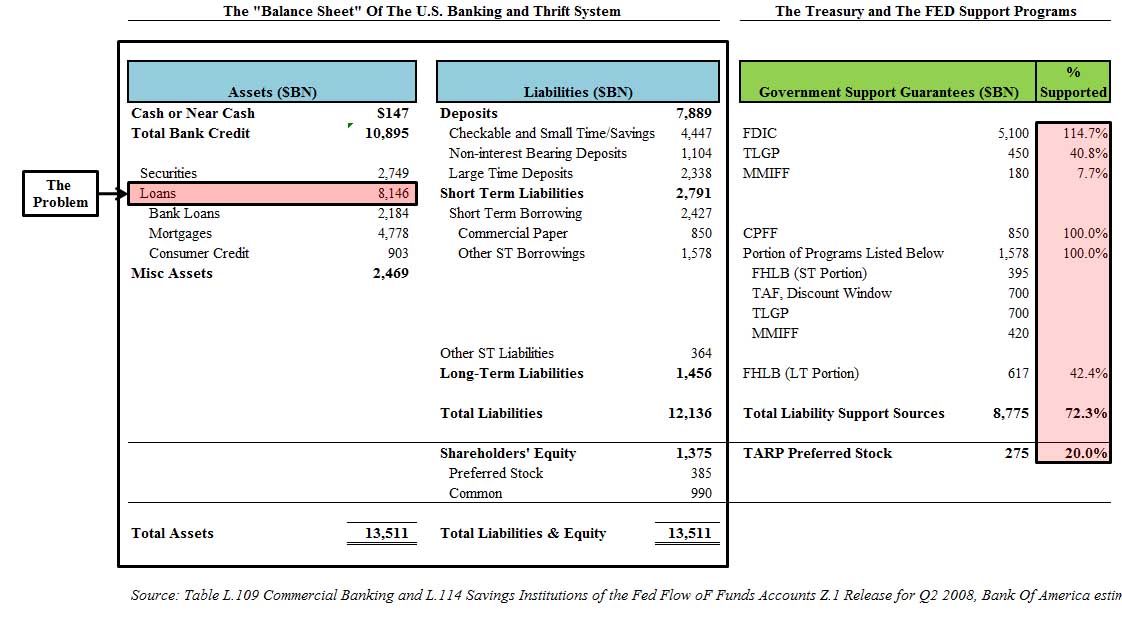

The U.S. Banking System’s Terrifying Balance Sheet

This is a spectacularly good piece of information design, from Tyler at Zero Hedge. It repays a lot of looking at, and manages to encapsulate both the scale of the US banking system and the scale of the solutions which have been announced or implemented to date. Click to enlarge:

{kind=link}

On the asset side of the US banking system’s balance sheet, the $4.8 trillion in mortgages is a problem — but there’s another $3.1 trillion in bank loans and consumer credit which is looking increasingly shaky. Against that there’s less than $1 trillion in common stock, supporting over $12 trillion in liabilities.

Meanwhile, Tyler has neatly lined up the government’s support programs along with the relevant parts of the right-hand side of the banking system’s balance sheet. Add them all up, and they come to just over $9 trillion, or 67% of the banking system’s total assets. It’s an absolutely astonishing amount of support, and it brings home the scale of the problem facing the government.

In a nutshell, the problem is the classic one: on the left-hand side nothing is right, and on the right-hand side nothing is left, at least absent government intervention. Says Tyler:

As the government has the best information about the true sad state of affairs, it is likely that as more and more information about the weakness of the financial system comes to light, more of these support guarantees will become utilized to their full extent. This also means that the asset side of the balance sheet is potentially “inflated” by almost 75% and the net result could be the most dramatic collapse in a banking system’s assets in recorded history as over $8 trillion in “assets” are reevaluated.

This doesn’t need to be probable to be terrifying: it just needs to be possible. And Tyler’s point is that the government has put all of these programs in place precisely because it’s possible. So: fear is entirely rational here.

——-

So far the article from a well known blogger (Felix Salmon, who got the info from ‘Tyler Durden’, another blogger). However, he indicates that all of the outstanding loans ($8+ Trillion!) are potential problems. That really is hard to believe, actually, let us rephrase that, this is nonsense.

This assumes that potentially, nobody pays anything (interest and principle) on their consumer credit or mortgage. We really cannot perceive any situation where that is near likely to happen.

Yes, there are numerous people behind with their monthly payments, and others who have stopped paying altogether, but to assume total default, well, how is that going to happen?

So in the end, this amounts to scaremongering. Which is exactly what we don’t need right now.

Agreed, at this point in the housing crisis the majority of bad mortgages have already been picked off the lowest hanging branches.

This would leave me to believe that a high percentage of the remaining mortgages are owned by individuals/groups that are unlikely to default.

People say crazy things to get attention, like one economist saying that there would be blood shed before this financial crisis is over. I think you have just posted another example of one of these people looking for attention.

Maybe we need fear mongering to give those bankers and regulator a motivation to do the right thing for a change. Lets not forget in the last decade or even more recent current events: I know there are “INVESTOR guidelines” and rules: SEC, FTC, FDIC, FNMA, TARP,

Freddie MAC and an even more powerful and ignored absolute rule of INTEGRITY.

I think that people are just tired of hearing all the excuses and finger pointing by these out-of-touch-with-reality millionaire investors, regulators, and bank executives saying there is nothing that they can do. From Enron, Martha Steward, the Keating Five Inquiry to Bernard Madoff: no dis-respect, but current history and our current economy shows me that banks and regulators do what ever they want to do.

My rhetorical question: who do consumers turn to for our STRESS test and bail out money?

Let’s face it, if all the rules were followed we would not be facing such an economic catastrophe. I have been looking for work for months now , but it is very difficult raising two teenagers as a single parent in this economic environment. So there is a cycle defaulting loan on the near horizon I think more than what is being predicted by the so call expert economists. You a can only TAX the working class so much before it begins to collapse and criminality [ blood shed ] begins to increase in response.

Lets wake up people and use some common sense – here! That is what has been missing in this economic fiasco for some time now and we are seeing the repercussions. Lets stop and look at these bankers for a moment: e.g. the AIG executive who in the midst of this world renowned Global fiasco with 24/7 news coverage and after receiving Tax payer bail out money had the nerve to reward his executive staff with our money – now when the President of the US has to step in to admonish a so called professional steward of finances to have those that were rewarded for a failed company to give the money back we are in bad shape!

I think this is a culture of millionaires who are spoiled and out of touch. Don’t get me wrong if you work hard and make money honestly and with integrity you deserve all that you earn…but to do and practice what these bankers, regulators and investor have done to us abusing the public trust to the extent that people are loosing not only there jobs, but there children college funds, retirement portfolios and dreams of a prosperous and relaxed future in senior years shows us and historians that change is needed. SO, MODERATOR PLEASE, DON’T DOWN PLAY THE REALITY OF THESE TROUBLING TIMES. THAT IS THE PROBLEM…we all need to be aware so that we can focus on the REAL problem and change it. Lets stop coddling these bankers and start replacing them with people with integrity and morals. Sorry if I offend anyone…I am a NY’er and call it the way I see it.

I don’t think we’re downplaying it, C Knight. In fact, we’re thinking the markets are due a correction and all the talk that things are back to normal is just that, talk.