Although some basically deny its existence, but the figures are heavily against them. Finally the SEC seems to be stepping up the plate..

Short Sellers Get the Squeeze

Trader Mark

Part of this article in the Wall Street Journal is about the steps taken to “take back” land from the short sellers; that is not the part I am concerned with. What I simply hate(d) as an investor in mid cap and some small cap stocks was the complete lack of attention the SEC paid to naked short selling. Short selling on its own is a positive; but naked short selling (selling shares that don’t even exist) is essentially a fraud. The reality is many of the big players whose prime broker were the Merrill Lynchs (MER), Goldman Sachs (GS), Lehman Brothers of the world – engaged in this. When pressed on this, the brokerages (and their institutional buddies) insisted its an overblown issue… certainly very rarely did a hedgie sit day after day shooting against a defenseless small cap stock as its personal plaything. Nope – all in your imagination folks.

Finally the SEC decided to step up to the plate …. why you might ask? Because the tables got turned on the same players who facilitated the short selling. Government Sachs and Morgan Stanely (MS) were threatened by the same ploys that year after year people winked winked about. But once the gun was turned on them; the CEO of Morgan Stanley was on the phone with the Administration and SEC and “this has to be stopped”. Just another example of how important it is being part of The Club. [Sep 15, 2008: SEC Finally Gets Around to Addressing Naked Short Selling?]

Well it’s taken catastrophe and carnage across Wall Street but maybe, just maybe the SEC plans on doing it’s job. There appear to be plans to strengthen action against naked short selling – sadly there are already regulations against this on the books but they appear to be so loose and very few respect it. There are entire lists of stocks on each exchange filled with stocks that are targets of this ploy, but nothing is done about it. We’ll see if there is any teeth to this new plan – but without regulation rules are meaningless.

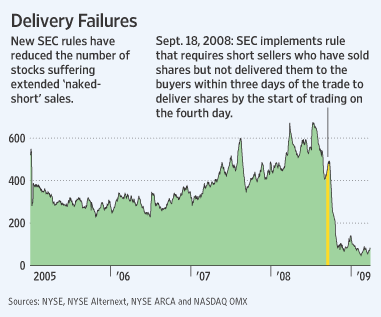

To show what a farce it has been all these years when the big honchos (who have profited frankly – illegally – from naked short selling) denied (a) it was happening or (b) it was so minor as to be nothing more than a nuisance or (c) something that was just a clerical situation (failure to deliver) and there was no way to really fix it, I’d like to present the graph below which shows an absolute free fall in number of “delivery failures” (the excuse du jour).

See, the Wild Wild West can indeed be fixed when the “in bed with the outlaws” sheriff has a reason to clean it up. Unfortunately it took the potential obliteration of the two biggest investment banks for it to be addressed. It is funny because some CEO’s such as Overstock.com’s (OSTK) Patrick Byrne were made out to be “loonies” for claiming such illegal manipulation was taking place. Again, short selling is fine; naked short selling is gaming the system.

Via WSJ

- Securities regulators and some financial firms are making it more difficult for investors to pile on when stocks are falling and further drive down prices. The Securities and Exchange Commission, facing years of criticism, has begun to crimp the ability of traders who bet against stocks to depress prices by selling millions of shares they don’t possess, known as naked short selling. And some financial firms have cut back on lending to traders who want to bet against stocks.

- The result: The number of stocks in which big chunks of shares haven’t properly been delivered to investors has plummeted, to a daily average of 79 in the three months ending in March from 529 in the first nine months of 2008, according to an analysis of trading data from major stock exchanges.

- Critics say short sellers, with the aid of brokerage firms, cause these delivery failures by shorting stocks without first borrowing shares, as required by securities law. Such activity drives down stocks by adding to the selling pressure.

- The moves come as the SEC meets Wednesday to discuss further potential restrictions on short sellers. These include reinstating the “uptick rule,” which until 2007 had required short sellers to wait for a rise, or uptick, in a stock’s price before placing their bet that it would go down.

- Critics say such trading by short sellers roiled stocks last year by swamping the market with sales that characterized the 2008 market volatility. Amid that turmoil, the SEC closed loopholes that had allowed sold shares to go undelivered.

- Despite the reductions in delivery failures, critics say the SEC took too long to act forcefully and still hasn’t gone far enough because failures still occur. “The majority of these failures-to-deliver are not the result of honest mistakes or bad processing,” former SEC commissioner Roel Campos wrote in a letter posted on the SEC’s Web site. “Rather, these companies are instead targets of illegal and manipulative trading, with intentional failures-to-deliver used by traders to extract profits as the share price plummets.”

- The SEC first attempted to address the problem in 2005, with the implementation of Regulation SHO, which mandated “threshold securities” lists, daily compilations by exchanges of stocks that had suffered at least five consecutive days of delivery failures totaling at least 10,000 shares and at least a half a percent of their outstanding shares each day. Once a stock hit the threshold lists, traders were required to close out failed deliveries by the 13th day after the trade. But there were loopholes in the regulation, and there was no requirement to close out delivery failures of securities that weren’t on the lists. (i.e. toothless regulation that was nothing more than eye candy)

- The threshold lists averaged about 300 securities a day in the first two years after Regulation SHO was instituted. In 2007, the daily average climbed to 414. In the first nine months of 2008, as the markets and banks crumbled, the lists averaged 529 securities.

- Last summer and fall, the SEC issued emergency orders restricting the short sales of certain financial firms and tightening the requirements for deliveries. Most important, observers say, was a new rule requiring short sellers to close out any delivery failure by the open of trading on the fourth day after the trade. The number of securities on the threshold lists has since plummeted. (imagine that – its funny how that works)

- But stricter SEC delivery requirements may have instilled a new discipline in market participants. In the past, hedge-fund and bank executives said, brokers were quick to tell clients not to worry about finding borrowed shares to sell short, even if there was some risk that they wouldn’t be able to find and deliver the stock.

And if you are wondering why it took so long to turn a “paper regulation” into something “effective” – it simply goes back to the same problem at the root at almost everything in the country. Politics – bought and paid for by those who pay for campaigns.

- Peter Chepucavage, a former counsel at the SEC who helped draft Regulation SHO, said the initial weakness of the rule and the years it took the SEC to stiffen it can be traced to the lobbying efforts of hedge funds and Wall Street.

- Brokerage firms “have made huge amounts of money” facilitating short selling, said Mr. Chepucavage, general counsel for Plexus Consulting Group, a Washington firm that advises nonprofit firms and broker-dealers. “They want and have argued strenuously for flexibility.”

Just like the housing bubble – it was great on the way up. But once the bazooka was turned at the brokerage firms?? They ran like scalded chimps to D.C. to make sure the rules were “effectively enforced” – the same rules they, and their clients – for years lobbied again.

Have to love Cramerica.